Stablecoin Yield in DeFi: The Complete Masterclass Guide (2026)

📋 En bref (TL;DR)

- $311 billion: the total market capitalization of stablecoins in March 2026, an all-time high reflecting the massive adoption of these digital assets pegged to the dollar or the euro.

- Average yield of 4 to 8% per year: DeFi protocols like Aave, Morpho, and Pendle generate returns on your stablecoins well above France’s government-regulated savings account, the Livret A (2.4%), or euro-denominated insurance funds (2.5%).

- 5 distinct yield sources: cash yield (tokenized Treasury bills), credit yield (lending), protocol yield (native savings rates), derivatives yield (delta-neutral strategies), and incentive yield (liquidity + emissions).

- 7 concrete methods: lending, liquidity provision, yield trading (Pendle), yield-bearing stablecoins, tokenized RWAs, looping, and yield aggregators.

- Aave V3 dominates lending with over $40 billion in TVL and rates of 4 to 6% on USDC/USDT, followed by Morpho Blue ($10 billion) and Compound V3 ($4 billion).

- Yield-bearing stablecoins are booming: sUSDe (Ethena), sDAI (MakerDAO), stkGHO (Aave), USDY (Ondo), USDf (Usual), and the brand-new EarnUSD from Lido (March 2026).

- $10,000 invested over 5 years: approximately $12,700 with a traditional savings account versus $14,800 with a diversified DeFi strategy at 8% — that’s $2,100 more.

- Risks do exist: smart contract, depeg, liquidation, regulatory, oracle, and governance risks. Transparency about these risks is essential before investing.

- Strategies tailored to every level: beginner (4-6% with simple lending), intermediate (6-10% through diversification), advanced (10-20% with Pendle and looping).

- Fibo simplifies everything: DeFi yield in 2 clicks, no gas to manage, no seed phrase, with swap fees of 0.25% — 3.5 times cheaper than MetaMask.

Introduction: Why Generate Yield on Stablecoins?

Generating yield on stablecoins in DeFi delivers between 4 and 8% per year on assets whose value remains stable — two to three times more than the best traditional savings products. It is now one of the most practical and accessible applications of decentralized finance.

Stablecoins are no longer just a transit tool between two trades. In March 2026, their total market capitalization exceeds $311 billion, and their annual transaction volume has reached $46 trillion — surpassing Visa’s. These numbers reflect a reality: stablecoins have become the financial infrastructure of DeFi.

Meanwhile, traditional savings options offer modest returns. In France, the Livret A — the government-regulated, tax-free savings account — caps out at 2.4% (and is expected to drop to 1.7% in February 2027, according to the Banque de France). Euro-denominated insurance funds average 2.5%. Standard savings accounts barely exceed 0.5%. In the US, high-yield savings accounts offer 4-5% at best, while traditional savings accounts hover near 0.5%. Inflation, though declining, continues to erode the purchasing power of traditional savings.

Faced with this situation, DeFi offers a credible alternative. Protocols like Aave, Morpho, and Pendle let you put your stablecoins to work with yields of 4 to 12% — or even more for advanced strategies — all while maintaining liquidity. No lock-up periods, no banking intermediary, no hidden fees.

This guide is designed as a comprehensive masterclass. It covers yield sources, methods, protocols, strategies by experience level, risks, and mistakes to avoid. Whether you’re discovering DeFi or looking to optimize an existing portfolio, you’ll find actionable and up-to-date information here.

Stablecoins: A Quick Refresher

A stablecoin is a digital asset whose value is pegged to a fiat currency (dollar, euro) or a basket of assets. They combine the stability of traditional currencies with the programmability and accessibility of blockchain.

Before discussing yield, here’s a refresher on the main stablecoins used in DeFi:

USDC (Circle) — The reference stablecoin for institutional DeFi. Issued by Circle, fully backed by dollar reserves and US Treasury bills, audited monthly by Deloitte. Market cap: approximately $60 billion. Available on more than 15 blockchains. It’s the most widely used stablecoin in lending and liquidity protocols.

USDT (Tether) — The oldest and largest stablecoin by market cap, with over $140 billion. Ubiquitous on centralized exchanges and increasingly integrated into DeFi. Its reserves, long criticized, are now attested quarterly by BDO Italia. USDT remains essential for liquidity, even though USDC is often preferred in DeFi for its transparency.

DAI / USDS (MakerDAO / Sky) — The first decentralized stablecoin, generated through collateralized debt positions (CDPs). In 2024, MakerDAO rebranded to Sky Protocol and DAI became USDS, but DAI remains widely used. Its savings version, sDAI (or sUSDS), offers native yield via the DSR (Dai Savings Rate).

USDe (Ethena) — The synthetic stablecoin that disrupted DeFi in 2024-2025. Backed by a delta-neutral strategy (long stETH / short ETH futures), USDe generates yield from the funding rates of derivatives markets. Its staked version, sUSDe, offers between 5 and 15% depending on market conditions. Market cap: approximately $6 billion.

EURC (Circle) — Circle’s euro stablecoin, MiCA-compliant. Still underutilized in DeFi compared to dollar stablecoins, but growing rapidly thanks to the European regulatory framework. Available on Ethereum, Base, Solana, and Avalanche.

Where Does the Yield Come From? The 5 Sources of Yield

Yield on stablecoins in DeFi comes from five distinct sources, each with its own risk/return profile. Understanding these sources is essential for evaluating whether a displayed rate is sustainable or too good to be true.

Too many guides just list protocols without explaining where the money comes from. Yet, that’s the fundamental question. If you don’t understand the source of the yield, you can’t assess its sustainability or its risks. Here’s a classification framework in five categories.

1. Cash Yield — Tokenized Treasury Bills (3.5-5%)

Cash yield comes directly from the returns of traditional financial assets — primarily US Treasury bills (T-Bills) — tokenized on the blockchain. It’s the simplest yield source to understand and the least risky in DeFi terms.

Protocols like Ondo Finance (USDY), BlackRock (BUIDL), and Mountain Protocol (USDM) purchase Treasury bills and redistribute the interest to stablecoin holders. The yield is predictable (it tracks the Fed funds rate) and the source is perfectly identifiable.

Typical rate: 3.5 to 5% APY, directly correlated with the Fed’s interest rates.

Main risk: falling interest rates (if the Fed cuts rates, yield decreases proportionally).

2. Credit Yield — DeFi Lending (3-8%)

Credit yield is the return earned by lending your stablecoins to other users via lending protocols. It’s the oldest and most battle-tested model in DeFi. You deposit your USDC into a lending pool (Aave, Morpho, Compound), and borrowers pay interest to use them.

The rate fluctuates based on supply and demand. When the market is bullish and borrowing demand surges, rates go up. In calm markets, they come back down. It’s an organic yield, generated by real economic utility.

Typical rate: 3 to 8% APY depending on the protocol and market conditions.

Main risk: smart contract risk of the lending protocol and theoretical pool insolvency in case of liquidation failure.

3. Protocol Yield — Native Savings Rates (4-7%)

Protocol yield comes from mechanisms built directly into the design of a stablecoin or protocol. MakerDAO’s DSR (Dai Savings Rate) is the foundational example: revenue generated by the protocol (stability fees, reserve investments) is redistributed to depositors.

Other examples include Ethena’s sUSDe (yield from delta-neutral positions), Aave’s stkGHO (staking rewards for the GHO stablecoin), and Lido’s EarnUSD (launched in March 2026), which combines staking yield with optimization strategies.

Typical rate: 4 to 7% APY, relatively stable since it’s tied to protocol revenue.

Main risk: dependence on the economic health of the issuing protocol and governance risk.

4. Derivatives Yield — Derivatives Strategies (5-12%)

Derivatives yield comes from exploiting spreads in crypto derivatives markets. The most well-known strategy is Ethena’s: buy stETH (long ETH exposure) and simultaneously sell an ETH futures contract (short exposure), creating a delta-neutral position. The yield comes from funding rates that long positions pay to shorts in a bull market.

Hyperliquid HLP uses a similar mechanism by market-making on its own derivatives platform. These strategies are sophisticated but offer attractive returns.

Typical rate: 5 to 12% APY, but highly variable depending on market conditions.

Main risk: funding rates can turn negative in a bear market, generating losses instead of gains.

5. Incentive Yield — Liquidity + Emissions (4-25%)

Incentive yield combines multiple sources: trading fees earned by liquidity providers, governance token emissions (CRV, AERO, etc.), and sometimes temporary reward programs (points, airdrops).

It’s the most variable and potentially the highest yield. Providing liquidity on Curve, Aerodrome (Base), or Uniswap V3 generates trading fees. Protocols add token emissions to attract liquidity. Pendle even allows trading these future yields.

Typical rate: 4 to 25% APY depending on the pool, the chain, and active incentive programs.

Main risk: dilution of reward tokens (farming tokens that lose value), impermanent loss for liquidity pools, and the temporary nature of incentives.

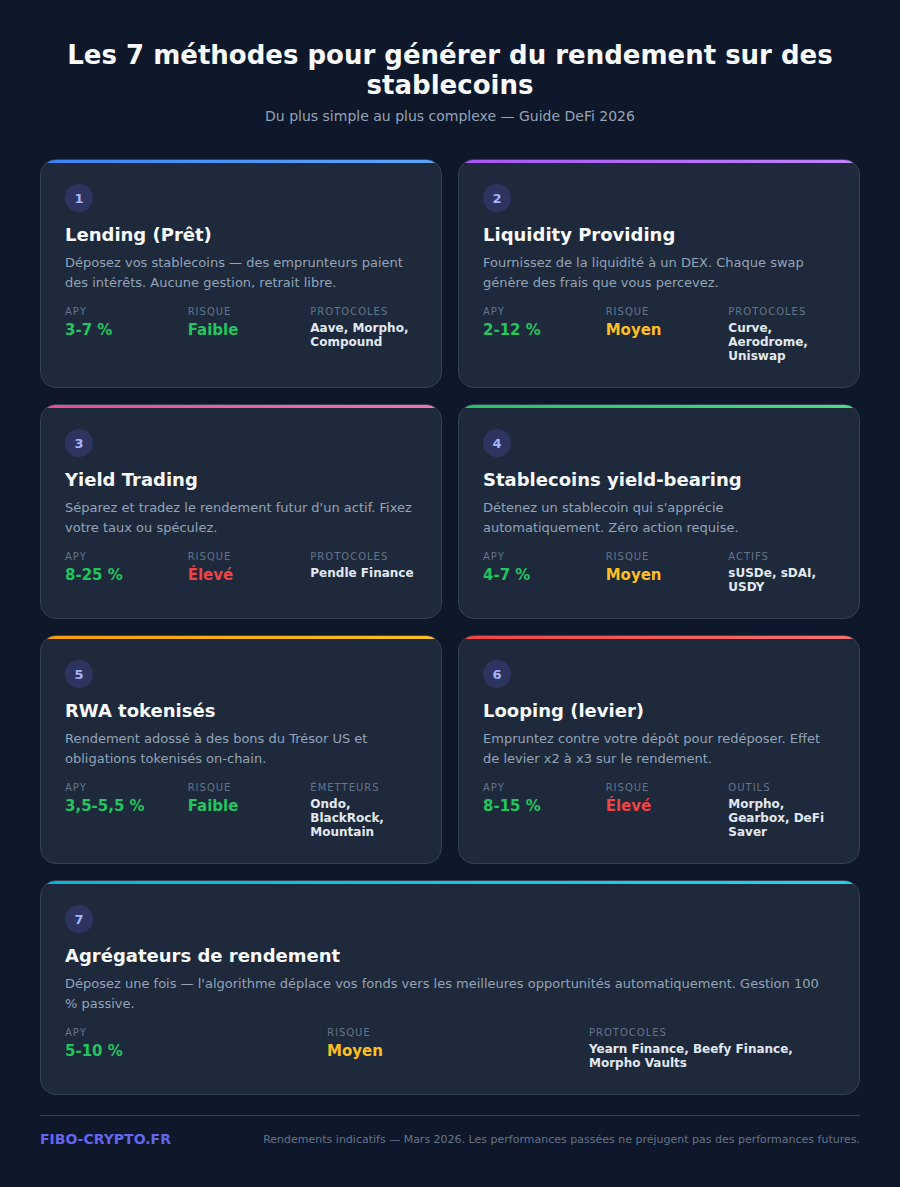

The 7 Methods to Generate Yield on Stablecoins

There are seven main methods to generate yield on stablecoins in DeFi, ranging from simple lending deposits (4-6%) to yield trading on Pendle (8-25%). Each method corresponds to a different level of complexity and risk profile.

1. Lending — The Simplest Method

Lending involves depositing your stablecoins in a lending protocol so other users can borrow them against collateral. It’s the most natural entry point into DeFi yield.

Aave V3 — The undisputed leader in DeFi lending with over $40 billion in TVL (Total Value Locked) across 14 blockchains. Aave V3 offers between 4 and 6% APY on USDC and USDT. The protocol has been operational since 2020, has undergone more than 30 security audits, and has never lost user funds on its main markets. It’s the benchmark for reliability.

Morpho Blue — The challenger that surged in 2025-2026 to reach approximately $10 billion in TVL. Morpho Blue stands out with its modular architecture: isolated markets where each parameter (collateral, oracle, LTV ratio) is defined independently. The result: rates often higher than Aave (4 to 8% on USDC) thanks to better capital efficiency. The protocol is particularly popular among intermediate and advanced users.

Compound V3 — The historic pioneer of DeFi lending with approximately $4 billion in TVL. Compound V3 (Comet) simplified its architecture by supporting only one borrowable asset per market (typically USDC). Rates are more modest (3 to 5%) but the protocol benefits from the longest track record in the sector.

Lending is ideal for getting started: you deposit, earn interest, and withdraw whenever you want. No impermanent loss, no management complexity. The risk is limited to the protocol’s smart contract.

2. Liquidity Provision — More Yield, More Complexity

Providing liquidity (LP) involves depositing pairs of tokens into decentralized trading pools. Traders pay fees to swap, and those fees are redistributed to liquidity providers.

Curve Finance remains the reference platform for stablecoin pools (USDC/USDT, USDC/DAI, etc.). Its AMM (Automated Market Maker) is optimized for correlated assets, which minimizes impermanent loss. Returns range from 2 to 8% in trading fees, with CRV emissions added on top for boosted pools.

Aerodrome (Base) is the dominant DEX on Coinbase’s Base blockchain, with stablecoin pools offering between 4 and 23% APY thanks to generous AERO token emissions. The growth of the Base ecosystem in 2025-2026 has made Aerodrome one of the most attractive DEXs for stablecoin yield.

Uniswap V3 offers concentrated liquidity pools: you choose a price range within which your liquidity is active. For stablecoin pairs (USDC/USDT for example), a narrow range around 1:1 maximizes the fees captured. However, the active management required makes this method less passive than lending.

Impermanent loss on stablecoin pools is generally low (the assets stay close to their peg), but it’s not zero in case of a temporary depeg. This is a point to watch.

3. Yield Trading on Pendle — The Most Innovative Method

Pendle is a protocol that allows you to separate and trade the future yield of an asset. It’s the most significant DeFi innovation of 2024-2025, and its adoption continues to grow in 2026.

The concept: when you deposit a yield-bearing asset (like Ethena’s sUSDe), Pendle separates it into two components:

- PT (Principal Token) — Represents the capital. You buy a PT at a discount and receive the full value at maturity. It’s the equivalent of a zero-coupon bond. If a PT USDC is priced at $0.94 with a 6-month maturity, you earn 6% by holding it until expiry. Fixed, predictable yield — no surprises.

- YT (Yield Token) — Represents the future yield. It’s a leveraged bet on yield: if rates go up, the YT gains value. If rates drop, it loses value. Highly speculative but potentially very profitable.

Rates on Pendle range from 8 to 25% APY depending on the assets and maturities. The PT strategy is particularly appealing for investors who want a guaranteed fixed yield over a given period — a rarity in DeFi.

4. Yield-Bearing Stablecoins — Built-In Yield

Yield-bearing stablecoins are stablecoins whose value increases automatically through a built-in yield mechanism. You hold them, they appreciate in value. No need to deposit into a third-party protocol.

sUSDe (Ethena) — 5 to 6% APY. The staked version of USDe. Yield comes from the funding rates of Ethena’s delta-neutral positions. One of the most popular yield-bearing stablecoins with over $5 billion in TVL.

sDAI / sUSDS (MakerDAO / Sky) — 4 to 6% APY. The DSR (Dai Savings Rate) redistributes protocol revenue (stability fees, RWA income) to depositors. Rate set by governance, historically stable.

stkGHO (Aave) — 4 to 5% APY. Aave’s GHO stablecoin can be staked to receive rewards. The rate is lower than other options but benefits from Aave’s credibility.

USDY (Ondo Finance) — 3.5 to 4% APY. Backed by US Treasury bills and bank deposits. It’s the most “TradFi” yield-bearing stablecoin: regulated, transparent, with a perfectly identifiable yield source.

USDf (Usual) — 6 to 7% APY. The Usual protocol redistributes returns from its reserves (T-Bills, short-term bonds) and adds incentives via its USUAL token. One of the highest yields in the category.

EarnUSD (Lido) — Launched in March 2026. Lido, the leader in Ethereum liquid staking, enters the yield-bearing stablecoin market. EarnUSD combines ETH staking yield with optimization strategies. Rates are still to be confirmed over time, but the first weeks show competitive rates. One to watch as a major 2026 innovation.

5. Tokenized RWAs — The Bridge to Traditional Finance

Tokenized Real World Assets (RWAs) are traditional financial assets — Treasury bills, bonds, real estate — represented as tokens on the blockchain. They offer real-world yield with DeFi composability.

Ondo USDY — Already mentioned above, it’s the leader in tokenized T-Bills accessible to the general public.

BlackRock BUIDL (BUILD) — BlackRock’s tokenized fund, from the world’s largest asset manager. BUIDL invests in short-term Treasury bills and distributes interest daily. With over $1.5 billion in assets, it’s the ultimate institutional validation of tokenized RWAs. Primarily accessible to qualified investors via Securitize.

Mountain USDM — A yield-bearing stablecoin backed by T-Bills, rebasing daily (the quantity of tokens in your wallet increases every day). Rate of 3.5 to 4.5% APY.

Tokenized RWAs are particularly appealing for investors seeking predictable yield with minimal DeFi risk. The yield source is clear and auditable.

6. Looping — Yield Amplification

Looping (or leverage looping) involves depositing a stablecoin as collateral, borrowing another stablecoin, redepositing the borrowed amount, and repeating. Each loop amplifies the base yield — but also the risk.

Concrete example: you deposit 10,000 USDC on Morpho at 5% APY. You borrow 7,000 USDT at 3% (70% LTV). You redeposit the 7,000 USDT at 5%. You borrow 4,900 USDT… and so on. With 2.5x leverage, your effective yield goes from about 5% to about 10% — but you also pay borrowing interest and are exposed to liquidation risk if the spread tightens.

Looping tools: Morpho (isolated markets facilitating leverage), Gearbox (automated composable leverage), DeFi Saver (automation with stop-loss). Interfaces like Instadapp or Contango simplify the process into a single transaction.

Looping is reserved for advanced users. Liquidation risk exists even between stablecoins (in case of a temporary depeg), and gas fees across multiple loops can be significant on Ethereum mainnet. Prefer L2s (Arbitrum, Base, Optimism) to reduce costs.

7. Yield Aggregators — Passive Optimization

Yield aggregators automate the search for and optimization of the best rates. You deposit your stablecoins, and the aggregator dynamically allocates them to the most profitable protocols.

Yearn Finance V3 — The pioneer of yield vaults. Yearn deploys automated strategies (lending, LP, farming) and reallocates funds based on opportunities. Stablecoin vaults typically offer 4 to 8% APY. 10% performance fee.

Morpho Vaults — Vaults curated by risk managers (like Gauntlet, Steakhouse, Block Analitica) that automatically allocate to the best Morpho Blue markets. It’s the most popular option in 2026 for optimized yield with professional risk management.

Beefy Finance — The quintessential multi-chain aggregator, present on more than 25 blockchains. Beefy auto-compounds farming rewards and simplifies access to yield strategies across all chains, including the newest ones (Base, Scroll, zkSync).

Aggregators are an excellent trade-off between yield and simplicity. You delegate the complexity while retaining custody of your funds (the smart contracts are non-custodial). However, risk stacks: aggregator smart contract risk + underlying protocol risk.

Detailed Protocol Comparison

In March 2026, Aave V3 remains the most reliable stablecoin yield protocol with $40 billion in TVL and no major incidents, while Morpho Blue offers the best rates (4-8%) thanks to its modular architecture. The choice between protocols depends on your priority: security, yield, or simplicity.

Lending Protocols

Aave V3

TVL: ~$40 billion | USDC APY: 4-6% | Chains: Ethereum, Arbitrum, Optimism, Base, Polygon, Avalanche, BNB, Scroll, zkSync, Metis, Gnosis, Fantom, Harmony, Celo | Audits: 30+ (OpenZeppelin, Trail of Bits, Sigma Prime, Certora) | Track record: since 2020 | Note: the most battle-tested protocol in DeFi.

Morpho Blue

TVL: ~$10 billion | USDC APY: 4-8% | Chains: Ethereum, Base | Audits: 5+ (Spearbit, Cantina, Trail of Bits) | Track record: since 2024 | Note: isolated markets, better capital efficiency, vaults curated by professionals.

Compound V3

TVL: ~$4 billion | USDC APY: 3-5% | Chains: Ethereum, Arbitrum, Base, Polygon, Optimism, Scroll | Audits: 10+ (OpenZeppelin, Trail of Bits) | Track record: since 2018 | Note: the pioneer of DeFi lending, simplified architecture in V3.

Liquidity Protocols

Curve Finance

TVL: ~$3 billion | Stable pool APY: 2-8% (+CRV) | Chains: Ethereum, Arbitrum, Optimism, Base, Polygon, Avalanche, Fantom, Celo | Audits: multiple (Trail of Bits, Quantstamp) | Track record: since 2020 | Note: AMM optimized for stablecoins, veCRV governance.

Aerodrome

TVL: ~$2 billion | Stable pool APY: 4-23% | Chain: Base only | Audits: 3+ | Track record: since 2023 | Note: dominant DEX on Base, generous AERO emissions.

Yield Trading

Pendle

TVL: ~$5 billion | PT APY: 8-25% | Chains: Ethereum, Arbitrum, BNB, Optimism, Mantle | Audits: 5+ (Spearbit, Ackee) | Track record: since 2021 (V2 since 2023) | Note: the only mature yield trading protocol, unique PT/YT innovation.

Yield-Bearing Stablecoins

Ethena (sUSDe)

TVL: ~$5 billion | APY: 5-6% (variable) | Chains: Ethereum, Arbitrum, Base | Audits: 3+ | Track record: since 2024 | Note: delta-neutral strategy, rates vary with market conditions.

MakerDAO/Sky (sDAI/sUSDS)

TVL: ~$3 billion | APY: 4-6% (DSR) | Chains: Ethereum, Gnosis | Audits: 20+ | Track record: since 2017 (DSR since 2019) | Note: the oldest DeFi protocol, decentralized governance.

Ondo Finance (USDY)

TVL: ~$800 million | APY: 3.5-4% | Chains: Ethereum, Solana, Arbitrum, Mantle, Sui, Aptos | Track record: since 2023 | Note: backed by T-Bills, regulated, the most institutional.

Aggregators

Yearn Finance V3

TVL: ~$800 million | Stable vault APY: 4-8% | Chains: Ethereum, Arbitrum, Optimism, Polygon, Base, Fantom | Audits: 10+ | Track record: since 2020 | Note: automated strategies, 10% performance fee.

Beefy Finance

TVL: ~$500 million | APY: variable | Chains: 25+ blockchains | Audits: 5+ | Track record: since 2020 | Note: multi-chain, auto-compound, broad coverage.

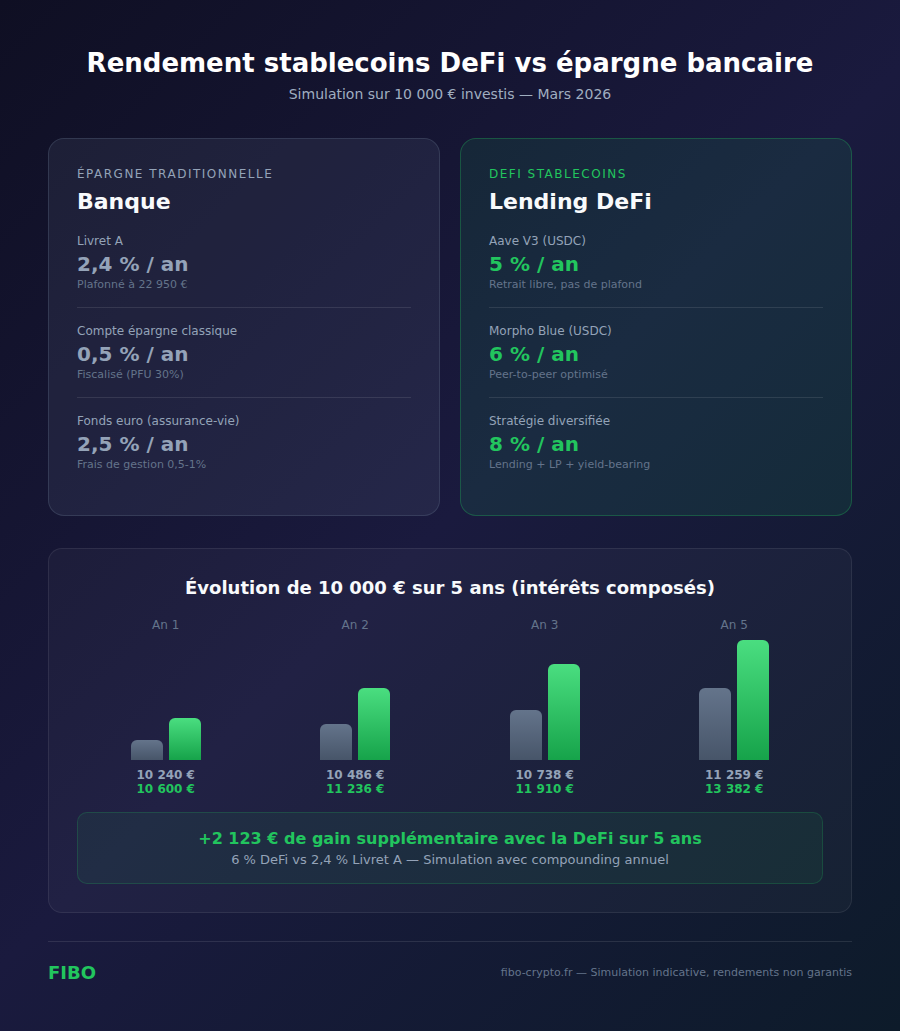

DeFi Yield vs Traditional Savings: A Striking Comparison

Over 5 years, a $10,000 DeFi investment at 8% APY generates approximately $4,800 in compound interest, versus $1,260 in a traditional savings account at 2.4%. The difference — over $3,500 — represents the opportunity cost of staying exclusively in traditional savings, even though DeFi carries risks that regulated savings products do not.

Comparative Returns

Let’s put the numbers side by side for a $10,000 investment over 5 years (annually compounded interest):

Traditional savings (France):

- Livret A — France’s government-regulated, tax-free savings account (2.4% in 2026, likely 1.7% in 2027): ~$11,260 after 5 years — i.e., +$1,260

- Standard bank savings account (0.5%): ~$10,253 — i.e., +$253

- Euro-denominated insurance fund (2.5%): ~$11,315 after 5 years — i.e., +$1,315 (before social contributions)

Traditional savings (US):

- High-yield savings account (4.5%): ~$12,462 after 5 years — i.e., +$2,462

- Standard savings account (0.5%): ~$10,253 — i.e., +$253

- 1-year Treasury bills rolled over (~4%): ~$12,167 — i.e., +$2,167

DeFi stablecoin strategies:

- Simple lending on Aave (5% APY): ~$12,763 — i.e., +$2,763

- Optimized Morpho Vault (6% APY): ~$13,382 — i.e., +$3,382

- Diversified Core+Satellite strategy (8% APY): ~$14,693 — i.e., +$4,693

The difference between a traditional savings account and a diversified DeFi strategy is over $3,400 over 5 years on a $10,000 initial investment. On larger amounts, the gap widens proportionally.

Essential Nuances

This comparison wouldn’t be honest without mentioning the fundamental differences:

What traditional savings offer that DeFi doesn’t:

- Deposit insurance (FDIC in the US up to $250,000; FGDR in France up to 100,000 EUR per institution)

- Tax exemptions on certain accounts (Livret A in France; Roth IRA in the US)

- Zero technical risk (no smart contracts, no wallet to manage)

- Clear and protective regulatory framework

What DeFi offers that banks don’t:

- Returns 2 to 4 times higher

- Instant liquidity (withdraw at any time, no cap)

- Total transparency (everything is verifiable on-chain)

- No deposit cap (the French Livret A is limited to 22,950 EUR)

- 24/7 access, no intermediary

The most pragmatic approach isn’t choosing one or the other, but diversifying: keep an emergency fund in a traditional savings account (precautionary savings), and allocate a portion of your available savings to DeFi for superior returns. The proportion depends on your risk tolerance and familiarity with the tools.

Tax Considerations

In France: DeFi yields are subject to the PFU (Flat Tax) of 30% (12.8% income tax + 17.2% social contributions). This tax applies upon conversion to euros. Even after taxes, a DeFi strategy at 8% gross yields approximately 5.6% net — still well above the Livret A (2.4% net, tax-exempt).

In the US: DeFi yields are generally treated as ordinary income, taxed at your marginal income tax rate (10-37% federal, plus state taxes where applicable). Crypto-to-crypto swaps may trigger capital gains events. Interest earned from lending protocols is typically taxable in the year it is received. Consult a tax professional for your specific situation.

It’s important to note that crypto taxation rules evolve regularly in both jurisdictions. Refer to the latest publications from your tax authority or consult a tax advisor for your personal situation.

Strategies by Experience Level

The best stablecoin yield strategy depends on your DeFi experience: a beginner should target 4-6% with simple lending on Aave, an intermediate user can reach 6-10% with a Core+Satellite approach, and an advanced user will optimize at 10-20% with Pendle and looping.

Beginner: 4-6% APY — Simple Lending

Profile: first DeFi experience, modest capital ($500-$5,000), security is the priority.

Objective: beat traditional savings without taking unnecessary risks.

Recommended strategy:

- Buy USDC on a regulated exchange (Coinbase, Kraken, Binance)

- Transfer to a non-custodial wallet (MetaMask, Rabby, or Fibo for simplicity)

- Deposit 100% into lending on Aave V3 — preferably on an L2 (Arbitrum or Base) to minimize gas fees

- Let interest accumulate automatically

Expected yield: 4-6% APY

Management time: 10 minutes for setup, then nothing (monthly check recommended)

Risk: low — only the smart contract risk of Aave (the most audited protocol in DeFi)

For absolute beginners, an even simpler alternative: buy sDAI or sUSDe directly. No need to interact with a lending protocol — the yield is built into the token. You hold it, it appreciates in value.

Intermediate: 6-10% APY — The Core + Satellite Approach

Profile: familiar with DeFi, medium capital ($5,000-$50,000), comfortable with 2-3 protocols.

Objective: optimize yield while diversifying risks.

Core + Satellite strategy:

- Core (50%) — Lending on a curated Morpho Vault or Aave V3. This is the stable base of the portfolio, with 4-6% APY and measured risk.

- Satellite 1 (30%) — Liquidity provision on Curve or Aerodrome (USDC/USDT or 3pool). Yield of 5-12% with farming rewards included.

- Satellite 2 (20%) — Yield-bearing stablecoin (sUSDe, USDf, or sDAI). Yield of 5-7%, no active management required.

Weighted expected yield: 6-10% APY

Management time: 1-2 hours per week to monitor positions and rebalance if necessary

Risk: moderate — diversification across 3+ protocols, limited exposure to each

Key rule: never put more than 30% of your capital in a single protocol. Diversification is your best protection against smart contract risk.

Advanced: 10-20% APY — Maximum Optimization

Profile: experienced in DeFi, significant capital ($50,000+), understands leverage and yield trading mechanics.

Objective: maximize yield with active risk management.

Multi-layer strategy:

- Pendle PT (40%) — Buy PT sUSDe or PT USDC with 6-12 month maturities. Fixed yield of 8-15% APY, no variation risk if held to maturity. This is the core of the advanced strategy.

- Morpho Looping (30%) — Leverage loop of 2x-2.5x on USDC/USDT with a 2-3% spread. Effective yield of 10-15% APY. Use DeFi Saver or Contango to automate and set stop-losses.

- Concentrated LP (20%) — Concentrated liquidity on Uniswap V3 or Aerodrome with active range management. Yield of 10-25% but requires regular monitoring.

- Pendle YT (10%) — Speculative position on rising rates. Potential for 2x-5x if rates increase, total loss possible if rates collapse. Deliberately limited allocation.

Weighted expected yield: 10-20% APY

Management time: 3-5 hours per week, daily monitoring of leveraged positions

Risk: high — leverage, liquidation risk, position complexity

Key rule for advanced strategies: always have an exit plan. Define in advance your liquidation thresholds, stop-losses, and rebalancing conditions. Yield is worth nothing if a liquidation wipes out your capital.

Due Diligence Checklist: 5 Checks Before Investing

Before depositing stablecoins in any DeFi protocol, five essential checks help evaluate the opportunity’s reliability and avoid unpleasant surprises. This checklist should become second nature for every DeFi investor.

1. Is the yield source identified?

This is the most important question. If you can’t explain in one sentence where the yield comes from, that’s a red flag. “Borrowers pay interest” (lending) is clear. “Trading fees are redistributed” (LP) is clear. “Yield is supported by community growth” is a red flag.

Ask yourself: who is paying this yield and why? If the answer isn’t obvious, dig deeper or move on.

2. Is the protocol audited, and how long has it existed?

Check the number of security audits (usually available on the protocol’s “Security” or “Docs” page). A single audit isn’t enough — benchmark protocols (Aave, MakerDAO, Compound) have 10 to 30. Also check the track record: a protocol that has operated for 2 years without incident has proven its resilience.

Platforms like DeFi Safety, DeFi Llama, and L2Beat provide risk scores and audit information.

3. What are the exit conditions?

Can you withdraw your funds at any time? Is there a lock-up period? A withdrawal delay (cooldown)? Early exit fees? Some protocols impose unlock periods of 7 to 21 days (like unstaking sUSDe, which requires a 7-day cooldown).

Make sure you know the exact conditions before depositing, especially if you might need liquidity quickly.

4. Are the reserves transparent?

For yield-bearing stablecoins and tokenized RWAs, reserve transparency is crucial. Circle publishes monthly attestations for USDC. Ethena publishes its collateral composition in real time. MakerDAO publishes its governance balance sheets.

Be wary of protocols that don’t publish proof of reserves or whose attestations are outdated. Transparency is a strong indicator of seriousness.

5. Is your risk concentrated?

Even the best protocol can experience an incident. Check your exposure: what percentage of your capital is on a single protocol? On a single chain? On a single type of stablecoin?

Rule of thumb: no more than 30% on one protocol, no more than 50% on one chain, and diversify between at least 2 different stablecoins (USDC + USDT, or USDC + DAI, for example).

Risks: What You Absolutely Need to Know

DeFi yield on stablecoins is not risk-free. Seven risk categories must be understood and managed: smart contract, depeg, liquidation, regulatory, counterparty, oracle, and governance. Ignoring these risks doesn’t make them disappear — understanding them allows you to mitigate them.

Smart Contract Risk

Every DeFi protocol runs on smart contracts — computer code deployed on the blockchain. A bug, security vulnerability, or logic error in the contract can result in a total loss of deposited funds.

This is the fundamental risk of DeFi. Even the most audited protocols are not immune. In 2023, Euler Finance lost $197 million despite 10 audits (funds were recovered after negotiation with the hacker). In 2022, the Wormhole bridge was exploited for $320 million.

Mitigation: favor protocols with numerous audits, a long track record, and an active bug bounty program. Diversify across multiple protocols.

Depeg Risk

A depeg occurs when a stablecoin temporarily or permanently loses its parity with its reference currency. In March 2023, USDC temporarily dropped to $0.87 following the Silicon Valley Bank collapse (where Circle held $3.3 billion in reserves). It recovered its peg within 48 hours, but investors exposed in LP positions suffered losses.

The most extreme case remains UST (Terra) in May 2022, which lost 99.99% of its value — but UST was an algorithmic stablecoin without sufficient collateral, a very different category from USDC or USDT.

Mitigation: diversify between stablecoins (don’t put everything in USDC or everything in USDT), favor stablecoins with audited and transparent reserves.

Liquidation Risk

Liquidation risk applies to strategies using borrowing (collateralized lending, looping). If the value of your collateral drops relative to your debt (even between stablecoins, in case of a depeg), your position can be automatically liquidated with a penalty (typically 5-10% of collateral).

Mitigation: maintain a comfortable collateralization ratio (LTV < 60% when the maximum is 80%), use automation tools (DeFi Saver) for emergency deleveraging.

Regulatory Risk

Stablecoin and DeFi regulation is evolving rapidly. In Europe, MiCA (Markets in Crypto-Assets) has imposed strict requirements on stablecoin issuers since June 2024: e-money licenses, segregated reserves, volume caps for non-euro stablecoins. In the United States, the debate on stablecoin regulation continues, with proposed legislation like the GENIUS Act and STABLE Act shaping the framework. Regulatory changes could affect the availability of certain stablecoins or protocols in your jurisdiction.

Mitigation: use compliant stablecoins (USDC, EURC), stay informed on regulatory developments, don’t ignore tax obligations.

Counterparty Risk

Some DeFi yields involve a counterparty: borrowers in lending, market makers in liquidity pools, custodians of tokenized RWAs. If the counterparty defaults, both yield and potentially capital are affected.

Mitigation: favor protocols with over-collateralization (Aave requires 120-150% collateral for every loan), verify the solidity of counterparties for RWAs.

Oracle Risk

DeFi protocols rely on oracles (Chainlink, Pyth, Redstone) to obtain asset prices. If an oracle provides an incorrect price (manipulation attack, technical failure), unjustified liquidations can occur or under-collateralized loans can be executed.

In October 2023, an oracle manipulation on an Aave market briefly caused abnormal liquidations on certain assets. The risk is rare but real, especially on less liquid markets.

Mitigation: check which oracle the protocol uses, favor protocols using decentralized multi-source oracles (Chainlink), avoid markets with illiquid assets.

Governance Risk

DeFi protocols are managed through decentralized governance (DAOs). Governance token holders vote on protocol parameters: rates, accepted collateral, upgrades. A poor governance decision can affect the protocol’s security or profitability.

Recent examples: controversial governance proposals at MakerDAO regarding reserve allocation, or debates over Aave’s risk parameters that temporarily affected rates.

Mitigation: follow the governance forums of protocols you’re invested in, diversify so you don’t depend on a single DAO.

The 7 Common Mistakes to Avoid

The majority of losses in stablecoin DeFi yield don’t come from hacks but from avoidable mistakes: chasing the highest rates without understanding the risks, failing to diversify, ignoring gas fees, or forgetting about taxes. Here are the seven most common mistakes and how to avoid them.

Mistake #1: Chasing the highest yield without understanding the source. A 50% APY is rarely sustainable. Always ask yourself: who is paying this yield? If the answer is “new depositors,” it’s a Ponzi scheme. Do this instead: understand the yield source before depositing, favor organic yields (trading fees, borrowing interest, Treasury bill revenue).

Mistake #2: Putting all your capital in a single protocol. Even Aave, the most reliable protocol, isn’t immune to incidents. Concentrating 100% of your capital in a single smart contract is an unnecessary risk. Do this instead: spread across a minimum of 3 protocols, with a maximum of 30% per protocol.

Mistake #3: Ignoring gas fees in your yield calculation. Depositing $500 of USDC on Aave via Ethereum mainnet can cost $10-30 in gas. If your annual yield is $25 (5% on $500), gas fees eat half of it. Do this instead: use L2s (Arbitrum, Base, Optimism) for small amounts, where fees are just a few cents.

Mistake #4: Not monitoring your leveraged positions. Looping and borrowed positions require active monitoring. A temporary stablecoin depeg can trigger a cascade of liquidations. Do this instead: set up alerts (DeBank, Zapper, protocol notifications), use DeFi Saver for automatic protections.

Mistake #5: Forgetting about taxes. DeFi yields are taxable. In France, the PFU flat tax of 30% applies. In the US, DeFi income is generally taxed as ordinary income at your marginal rate. Failing to report is illegal, and tax authorities have increasingly sophisticated tools to trace blockchain transactions. Do this instead: keep a record of all transactions, use a crypto tax tracking tool (Koinly, CoinTracker, TaxBit), file annually.

Mistake #6: Using unknown stablecoins for a few extra percentage points. An obscure stablecoin offering 2% more than USDC isn’t worth the depeg risk. Stick with established stablecoins with audited reserves. Do this instead: stick to the top 10 stablecoins by market cap, verify proof of reserves.

Mistake #7: Not having an exit plan. Knowing when to enter is easy. Knowing when to exit is what separates profitable investors from the rest. Do this instead: define withdrawal conditions in advance (if the rate drops below X%, if an audit reveals a problem, if TVL drops more than 30% in a week).

How to Choose the Right Strategy

Choosing the right stablecoin yield strategy depends on three factors: your risk tolerance, your available capital, and the time you can dedicate to management. There is no universal strategy — the best one is the one that fits your profile.

By Risk Tolerance

Conservative — Absolute priority on capital safety. Target 3-5% APY via simple lending on Aave V3 (L2) or tokenized RWAs (USDY, BUIDL via accessible funds). Accept lower yield in exchange for near-certainty of recovering your capital.

Moderate — Willing to accept measured risk for better returns. Target 5-8% APY with the Core+Satellite approach: base in lending, diversification in stablecoin LP and yield-bearing stablecoins. Diversification across 3-4 protocols limits the impact of an isolated incident.

Dynamic — Comfortable with complexity and DeFi risks. Target 8-15% APY with Pendle strategies (PT/YT), measured looping, and concentrated liquidity. Accept the possibility of temporary losses in exchange for higher yield.

By Available Capital

Less than $1,000 — Gas fees matter a lot at this scale. Stay on a single L2 (Base or Arbitrum), a single protocol (Aave V3), a single stablecoin (USDC). Simplicity maximizes net yield.

$1,000 to $10,000 — You can start diversifying across 2-3 protocols, still on L2. The Core+Satellite approach becomes relevant.

Over $10,000 — Multi-protocol and multi-chain diversification is justified. Advanced strategies (Pendle, looping) become worthwhile after fees. Ethereum mainnet becomes viable again as gas fees are amortized over larger capital.

By Available Time

Passive (less than 1 hour per month) — Simple lending (Aave, Morpho Vault) or yield-bearing stablecoins (sUSDe, sDAI). Deposit and forget, with a monthly check.

Semi-active (1-2 hours per week) — Core+Satellite with weekly rebalancing. Stablecoin LP with reward monitoring. Pendle PT with fixed maturity.

Active (daily) — Looping, concentrated LP, yield trading (Pendle YT), rate arbitrage between protocols. Requires monitoring tools (DeBank, Zapper) and configured alerts.

2026 Trends and Outlook

The year 2026 marks a turning point for stablecoin yield in DeFi: the supply of yield-bearing stablecoins has doubled in one year, tokenized RWAs are converging with TradFi, and MiCA regulation is restructuring the European market. Five major trends are shaping the sector’s future.

Lido’s EarnUSD Launch

In March 2026, Lido — the dominant liquid staking protocol with over $30 billion in TVL — launched EarnUSD, its yield-bearing stablecoin. It’s a strong signal: the largest DeFi protocol is entering the productive stablecoin market. EarnUSD combines Ethereum staking yields with optimization strategies, positioning Lido as a direct competitor to Ethena and MakerDAO in the stablecoin yield segment.

This launch could reshuffle the market by attracting a portion of TVL from existing protocols to the Lido ecosystem.

The Yield-Bearing Stablecoin Boom

The total supply of yield-bearing stablecoins has doubled between March 2025 and March 2026, growing from approximately $15 billion to over $30 billion. sUSDe (Ethena), sDAI (MakerDAO), USDY (Ondo), USDf (Usual), and now EarnUSD (Lido): each quarter brings a serious new entrant.

This trend reflects growing demand for “passive” yield — stablecoins that work without the user needing to interact with complex protocols. It’s the ultimate simplification of DeFi yield.

The RWA and TradFi Convergence

BlackRock BUIDL, Franklin Templeton BENJI, Ondo USDY, Hashnote USYC: traditional finance giants are increasingly tokenizing assets on blockchain. The tokenized RWA market now exceeds $12 billion.

This convergence blurs the boundaries between DeFi and TradFi. A user can now hold US Treasury bills via a token on Ethereum, receive interest automatically, and use that token as collateral in DeFi protocols. The composability of blockchain applied to traditional assets opens unprecedented possibilities.

MiCA’s Impact on the European Market

The MiCA (Markets in Crypto-Assets) regulation, fully in force since June 2024, imposes strict requirements on stablecoin issuers in Europe: e-money licenses, segregated reserves, volume caps for non-euro stablecoins. USDT is under pressure in the EU (Tether hasn’t obtained a MiCA license in most jurisdictions), while USDC and EURC (Circle, licensed in France) benefit from a regulatory advantage.

For European investors, MiCA brings both constraints (some stablecoins less accessible) and protections (transparency and reserve requirements). EURC could gain importance if DeFi protocols develop more euro-denominated pools.

L2s Are Lowering the Barriers

Layer 2 blockchains (Arbitrum, Base, Optimism, Scroll, zkSync) have reduced transaction fees on Ethereum from $10-50 to just a few cents. This cost reduction democratizes access to DeFi yield: an investor with $500 can now use Aave on Base without gas fees eating into their returns.

In 2026, the majority of stablecoin yield activity takes place on L2s. Ethereum mainnet remains relevant for large amounts (>$50,000) or exclusive protocols, but L2s have become the standard for individual users.

The Simplest Alternative: Fibo

Fibo is a non-custodial mobile app that lets you generate yield on stablecoins in DeFi in two clicks, without having to manage gas, seed phrases, or technical complexity. It’s the simplest gateway between your savings and DeFi yield.

If after reading this guide, the technical complexity still feels daunting, Fibo was designed exactly for you. The app directly integrates DeFi lending via Aave — the most reliable protocol on the market — and abstracts away all the technical complexity.

What Fibo simplifies:

- No seed phrase — Your wallet is secured via Privy (login with email, Google, or Apple + passkey). You retain custody of your funds without having to back up 24 words.

- No gas to manage — Fibo handles gas fees in the background. You pay gas with the token you’re using (no need to buy ETH separately).

- Transparent fees — 0.25% commission on swaps. That’s 3.5 times cheaper than MetaMask or Phantom (0.875%). No hidden fees, no deposit or withdrawal fees.

- Yield in 2 clicks — Deposit stablecoins, activate DeFi yield. Aave works for you in the background. Withdraw whenever you want, no lock-up period.

- Built-in multi-chain — Base, Arbitrum, Polygon, Ethereum, Solana, Bitcoin. You don’t have to choose the right chain or manually bridge your assets.

Fibo doesn’t replace the advanced strategies described in this guide. If you’re an experienced user looking for yield trading on Pendle or looping on Morpho, you’ll likely use dedicated interfaces. But for the majority of investors who simply want to put their stablecoins to work with a return above traditional savings, Fibo is the most direct solution.

The app is developed by ADVIJU INVESTISSEMENT, a French company registered as a PSAN (Digital Asset Service Provider) with the AMF (France’s financial markets authority).

Glossary

📚 Glossary

- APY (Annual Percentage Yield) : annualized rate of return that includes the effect of compound interest. A 5% APY means $10,000 generates approximately $500 in interest over one year (more with compounding).

- TVL (Total Value Locked) : total value of assets deposited in a DeFi protocol. It’s an indicator of trust and adoption — the higher the TVL, the more the protocol is used.

- Stablecoin : digital asset whose value is pegged to a fiat currency (dollar, euro) or a basket of assets. The main ones are USDC, USDT, DAI, and USDe.

- DeFi (Decentralized Finance) : a set of financial services (lending, trading, savings) running on blockchain via smart contracts, without banking intermediaries.

- Lending : decentralized lending mechanism where depositors lend their assets to borrowers via a smart contract, in exchange for interest.

- Smart contract : computer program deployed on a blockchain that executes automatically when predefined conditions are met. It’s the technical foundation of DeFi.

- Impermanent loss : temporary loss incurred by liquidity providers when the price ratio between the two assets in a pool changes. On stablecoin pools, this effect is generally minimal.

- Depeg : loss of parity of a stablecoin with its reference currency. A USDC that drops to $0.95 is experiencing a 5% depeg.

- Yield-bearing (stablecoin) : a stablecoin whose value increases automatically through a built-in yield mechanism (e.g., sUSDe, sDAI, USDY).

- RWA (Real World Assets) : traditional financial assets (Treasury bills, bonds, real estate) tokenized on blockchain for use in DeFi.

- Layer 2 (L2) : blockchain built on top of Ethereum to reduce fees and increase transaction speed. Examples: Arbitrum, Base, Optimism.

- DSR (Dai Savings Rate) : MakerDAO’s native savings rate, redistributing protocol revenue to sDAI/sUSDS holders.

- Delta-neutral : investment strategy that combines a long position and a short position on the same asset to neutralize price variation risk, capturing only the yield.

- Funding rate : periodic payment between buyers and sellers on perpetual futures markets. In a bull market, longs pay shorts — this is Ethena’s yield source.

- PT (Principal Token) : on Pendle, a token representing the capital of a yield-bearing asset. Bought at a discount, it reaches its face value at maturity — equivalent to a zero-coupon bond.

- YT (Yield Token) : on Pendle, a token representing the future yield of an asset. Allows speculating on rate movements with leverage.

- Looping : yield amplification strategy consisting of depositing an asset, borrowing against it, and redepositing the borrowed amount iteratively to create a leverage effect.

- Oracle : service that provides external data (prices, rates) to smart contracts on blockchain. Chainlink is the most widely used oracle in DeFi.

- MiCA (Markets in Crypto-Assets) : European regulation governing issuers of digital assets and stablecoins, in force since June 2024.

- Non-custodial : describes a wallet or service where the user retains exclusive control of their private keys and funds. No third party can access your assets.

- PFU (Flat Tax) : French tax regime applying a flat rate of 30% on capital gains from digital asset disposals. In the US, crypto gains are taxed as capital gains (short-term or long-term depending on holding period).

- AMM (Automated Market Maker) : algorithm that automatically manages trades in a liquidity pool, replacing the traditional order book. Used by Curve, Uniswap, Aerodrome.

Frequently Asked Questions

Frequently Asked Questions

What is the average stablecoin yield in DeFi in 2026?

The average stablecoin yield in DeFi in 2026 ranges between 4 and 8% APY for standard strategies (lending, yield-bearing stablecoins). Leading protocols like Aave V3 offer 4 to 6% on USDC and USDT, while more advanced strategies (Pendle, looping) can reach 10 to 20%. These rates vary based on market conditions and the protocol used.

Is it risky to generate yield on stablecoins?

Yes, risks exist. The main ones are smart contract risk (bugs in the protocol’s code), depeg risk (the stablecoin loses its parity), and liquidation risk (for leveraged strategies). However, these risks can be significantly reduced by choosing audited and battle-tested protocols (Aave, MakerDAO), diversifying across multiple protocols, and avoiding leveraged strategies if you’re a beginner. Simple lending on Aave V3 is considered the least risky option.

How do I easily generate yield on USDC?

The simplest method to generate yield on USDC is to deposit it in a lending protocol like Aave V3 on a Layer 2 (Arbitrum or Base) to minimize gas fees. The current yield is 4 to 6% APY. Alternatively, you can convert your USDC to sDAI (MakerDAO) or sUSDe (Ethena) for built-in yield without additional interaction. Apps like Fibo let you do this in two clicks from your mobile.

How does DeFi yield compare to traditional savings?

Traditional savings rates vary by country. In France, the Livret A (government-regulated savings account) offers 2.4% in 2026 (net of tax, government-guaranteed, capped at 22,950 EUR). In the US, high-yield savings accounts offer 4-5%. DeFi stablecoin yield ranges from 4 to 8% (gross, not guaranteed, no cap). After taxes, DeFi net yield is approximately 2.8 to 5.6% (depending on jurisdiction). DeFi offers higher returns but carries risks (smart contract, depeg) that insured savings accounts don’t have. The recommended approach is to combine both: traditional savings for your emergency fund, DeFi for yield optimization.

What are the best protocols for stablecoin yield in 2026?

The best stablecoin yield protocols in 2026, ranked by reliability and yield, are: Aave V3 ($40B TVL, 4-6%, the most reliable), Morpho Blue ($10B TVL, 4-8%, best capital efficiency), Pendle ($5B TVL, 8-25%, fixed yield via PT), Ethena/sUSDe ($5B TVL, 5-6%, passive yield-bearing), and MakerDAO/sDAI ($3B TVL, 4-6%, the oldest). The choice depends on your experience and risk tolerance.

Do I need to report DeFi yields for tax purposes?

Yes, DeFi yields are taxable in most jurisdictions. In France, they are subject to the PFU (Flat Tax) of 30% upon conversion to euros (12.8% income tax + 17.2% social contributions). Crypto-to-crypto swaps are not taxed until you convert to fiat currency. In the US, DeFi yields are generally treated as ordinary income, taxable in the year received. Crypto-to-crypto swaps may also trigger taxable events. It is recommended to use a crypto tax tracking tool (Koinly, CoinTracker, TaxBit) and file annually according to your jurisdiction’s requirements.

What is a yield-bearing stablecoin?

A yield-bearing stablecoin is a stablecoin whose value increases automatically through a built-in yield mechanism. Unlike lending where you deposit into a protocol, you simply hold the token to earn yield. Examples: sUSDe (Ethena, 5-6%), sDAI (MakerDAO, 4-6%), USDY (Ondo, 3.5-4%), USDf (Usual, 6-7%). It’s the most passive method to generate yield on stablecoins.

What is the minimum capital to start stablecoin yield farming?

You can start with as little as $50 to $100 using Layer 2s like Base or Arbitrum, where gas fees are just a few cents. However, for the yield to be meaningful, a capital of $500 to $1,000 is recommended. Below that, conversion fees (exchange to wallet) and potential gas fees significantly reduce net yield. For advanced strategies (looping, Pendle), a minimum of $5,000 is advisable to offset the complexity and fees.

What is the difference between APY and APR?

APR (Annual Percentage Rate) is the simple annual interest rate, without compounding. APY (Annual Percentage Yield) includes the effect of compound interest — interest that itself generates interest. For example, a 10% APR compounded daily yields an APY of approximately 10.52%. In DeFi, most protocols display APY because it better reflects the actual yield. The difference between APR and APY becomes more significant as the rate increases and compounding is more frequent.

Is DeFi yield on stablecoins passive income?

DeFi yield on stablecoins can be considered semi-passive income. Simple lending (Aave, Morpho) and yield-bearing stablecoins (sUSDe, sDAI) require very little management after the initial deposit — a monthly check is sufficient. However, advanced strategies (looping, concentrated LP, Pendle yield trading) require regular monitoring. The level of passivity depends on the chosen strategy. For truly passive income, favor simple lending or yield-bearing stablecoins.

Can you lose your capital with stablecoin yield farming?

Yes, capital loss is possible, although stablecoins reduce volatility risk. Loss scenarios include: a smart contract hack (total loss possible but rare on major protocols), a stablecoin depeg (loss proportional to the parity drop), or liquidation on a leveraged position (partial loss with penalty). However, simple lending on established protocols like Aave has never resulted in user fund losses on its main markets in over 5 years of operation.

Which blockchains should I use for stablecoin yield in 2026?

In 2026, the best blockchains for stablecoin yield are: Ethereum (the most secure, but high gas fees — for large amounts), Arbitrum (low fees, broad DeFi ecosystem with Aave, GMX, Pendle), Base (very low fees, Aerodrome and Morpho very active, backed by Coinbase), and Optimism (Velodrome ecosystem, Synthetix). For beginners, Base and Arbitrum offer the best accessibility-to-yield ratio thanks to fees of just a few cents and broad presence of major protocols.

Sources

The simplest way to buy, swap and manage your crypto

Join the first users and get priority access. No seed phrase, fees 3.5x lower, built-in DeFi yield.

Get early access →