Corporate Treasury and Crypto: How to Invest Wisely in 2026

📋 En bref (TL;DR)

- Proven trend: Strategy holds over 713,000 BTC in 2026, Tesla 11,500, Block 8,600 — corporate crypto treasury is now mainstream among major companies.

- Clear regulatory framework: In Europe, MiCA provides a harmonized framework for crypto-asset service providers (CASPs) since 2025. In the US, the FASB fair value standard (ASU 2023-08) applies from 2025.

- Defined accounting treatment: Crypto assets are classified as intangible assets under most frameworks, with impairment testing required. FASB now mandates fair value accounting.

- Prudent allocation recommended: Between 3% and 10% of surplus treasury, depending on the company’s risk profile and cash flow needs.

- DCA strategy preferred: Dollar Cost Averaging reduces volatility exposure for corporate buyers, as demonstrated by Block’s quarterly purchase approach.

- Complementary to traditional investments: Crypto doesn’t replace savings accounts or bonds but adds an asymmetric return component to a diversified treasury portfolio.

- Regulated platform required: Choose a licensed CASP (MiCA in Europe) or registered custodian with fund segregation and corporate-grade reporting.

Why are companies investing their treasury in crypto?

The silent erosion of idle cash

With savings account yields hovering between 1% and 3% across most developed economies, and inflation having fluctuated between 2% and 5% in recent years, uninvested cash loses purchasing power mechanically. Money market funds and term deposits often deliver real returns below zero after inflation. For a company holding $500,000 in surplus treasury, this translates into thousands of dollars in lost value annually.The corporate adoption precedent

Institutional adoption has reached a tipping point:- Strategy (MicroStrategy): With over 713,000 BTC on its balance sheet in 2026, the company has transformed its business model into a “Bitcoin Treasury Company.” Its stock has outperformed the S&P 500 since adopting this strategy.

- Tesla: Holds 11,509 BTC with a long-term hold policy after a partial sale in 2022.

- Block (Square): Approximately 8,600 BTC acquired progressively through a quarterly DCA strategy, demonstrating that a measured approach is viable for corporate treasury.

Diversification and asymmetric returns

Bitcoin has delivered an annualized return exceeding 50% over the past decade. Even with a modest 5% allocation, the impact on an overall treasury portfolio’s return profile can be significant — without jeopardizing the company’s financial stability.What is the regulatory and accounting framework?

Regulatory landscape: MiCA, SEC, and beyond

The regulatory environment for corporate crypto holdings has matured significantly:- Europe (MiCA): The Markets in Crypto-Assets regulation, fully effective since late 2024, establishes a unified framework across the EU. Crypto-Asset Service Providers (CASPs) must obtain authorization. In France, existing PSAN-registered firms have until July 1, 2026 to transition to MiCA licensing.

- United States: The SEC continues to develop oversight of digital assets. The approval of spot Bitcoin ETFs in 2024 has significantly legitimized corporate exposure to Bitcoin.

- International: Jurisdictions from Singapore to the UAE have established clear licensing frameworks, making cross-border compliance increasingly manageable.

Accounting treatment

The accounting landscape has evolved substantially:- FASB (US GAAP): ASU 2023-08, effective from fiscal years beginning after December 15, 2024, requires fair value measurement of crypto assets. This means both gains and losses are reflected in earnings, providing a more accurate picture of economic reality.

- IFRS: Crypto assets are generally classified as intangible assets (IAS 38), with impairment-only measurement. However, the IASB is monitoring developments and may adopt fair value approaches.

- French GAAP (PCG): Crypto assets held as investments are recorded as intangible assets (account 205x). Impairment losses reduce taxable income, but unrealized gains are not recognized until disposal.

Tax implications

Corporate taxation of crypto gains varies by jurisdiction:- France: Capital gains on crypto disposals are integrated into the corporate tax base and subject to the standard corporate tax rate (25% in 2026). No VAT applies to investment holdings.

- US: Treated as property for tax purposes. Capital gains rates apply upon disposal, with the new fair value accounting creating timing differences between book and tax treatment.

- EU: MiCA does not harmonize tax treatment — each member state applies its own corporate tax rules to crypto gains.

What allocation strategies work for corporate treasury?

Defining a coherent allocation

Most specialized advisors recommend allocating between 3% and 10% of surplus treasury — the cash that exceeds short-term working capital requirements. This range captures the upside potential of crypto assets without exposing the company to liquidity risk. Practical example: A mid-market company with $800,000 in surplus treasury could allocate between $24,000 and $80,000 to crypto assets, while keeping the remainder in liquid traditional instruments.Asset selection

- Bitcoin (BTC): The most institutional, most liquid, and most correlated to macro adoption. It is the primary choice for corporate treasury allocation.

- Ethereum (ETH): The second-largest by market cap, with an extensive DeFi ecosystem. Relevant for companies with technological affinity.

- Stablecoins (USDC, EURC): Pegged to fiat currencies, they allow exposure to the crypto ecosystem without volatility. Useful as a tactical position or for securing gains.

DCA vs lump-sum investment

For corporate buyers, Dollar Cost Averaging (DCA) — investing a fixed amount at regular intervals — is generally preferable to a single large purchase. It allows you to:- Average out the entry price over several months

- Reduce the risk of unfavorable timing

- Integrate purchases into a regular budgeting process

- Simplify accounting traceability

How to choose the right investment platform?

Platform selection is critical for a corporate investor. Here are the essential criteria:Regulatory licensing

Any platform used for purchasing or holding crypto assets must hold the appropriate regulatory license for your jurisdiction. In Europe, this means CASP authorization under MiCA. In France specifically, PSAN registration with the AMF is required (transitioning to MiCA by July 2026). This is not optional — it is a legal requirement.Key criteria for corporate clients

- Fund segregation: Your company’s assets must be separated from the platform’s own funds. In the event of provider insolvency, your assets remain your property.

- Insurance and secure custody: Cold storage, multi-signature wallets, insurance against theft and hacking.

- Accounting-ready reporting: The platform should provide statements compatible with your local accounting standards (PCG, US GAAP, IFRS) to facilitate your accountant’s work.

- B2B support: Dedicated account manager, corporate onboarding, KYB (Know Your Business) compliance.

- Liquidity depth: Ability to execute large orders without significant price impact (slippage).

Why investing in crypto through a PSAN registered with France’s AMF matters

FTX, Mt. Gox… Crypto scandals have cost investors billions. In France, the PSAN license guarantees a regulated framework: identity verification, fund segregation,…

2x cheaper fees. Up to 6% yield. No seed phrase. Fibo, the wallet you've been waiting for.

Get early access →What are the specific risks for a company?

Investing corporate treasury in crypto assets carries risks that must be quantified and managed:Volatility and balance sheet impact

Bitcoin can fluctuate 20–30% within weeks. Under impairment-only accounting (IFRS/PCG), a decline in value must be provisioned, directly impacting the fiscal year’s results — and potentially affecting dividend distribution capacity or bank lending covenants. Under FASB fair value rules, both gains and losses flow through earnings, creating income statement volatility.Reputational risk

Depending on the industry, crypto investment may raise questions from partners, clients, or investors. Transparent communication about the strategy and amounts allocated is recommended.Cybersecurity

Holding crypto assets exposes the company to hacking risks. Choosing a regulated platform with cold storage and insurance is essential. Multi-signature wallets add an additional layer of security.Liquidity risk

For major assets (BTC, ETH), liquidity is excellent. However, for small-cap altcoins, spreads can be significant — especially for large orders. A corporate treasury should stick to the most liquid assets.Regulatory evolution

The regulatory framework continues to evolve (MiCA implementation, potential FASB updates, SEC oversight). Regular legal monitoring is essential, ideally with counsel specialized in digital asset law.Traditional vs crypto investments: how do they complement each other?

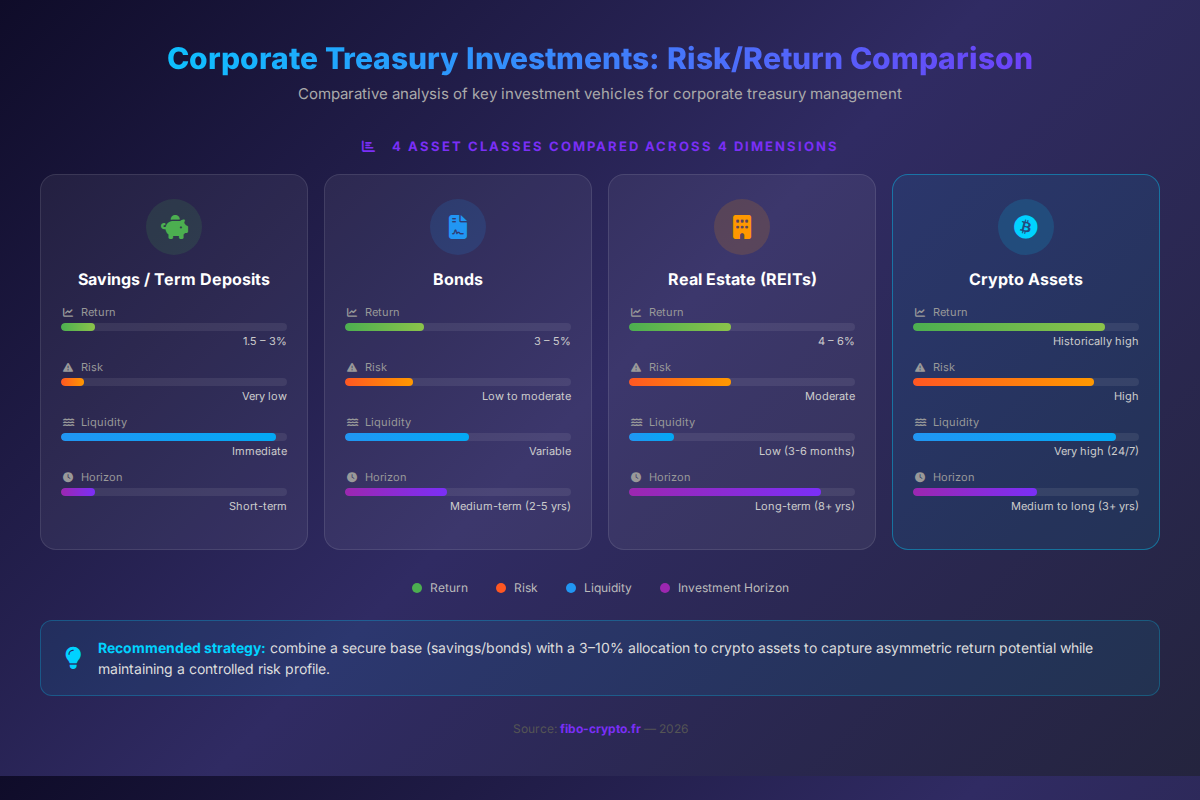

Crypto investment should not be viewed as an alternative to traditional instruments, but as a diversification complement. Here is a comparative overview:

| Criteria | Savings / Term Deposits | Bonds | Real Estate (REITs) | Crypto Assets |

|---|---|---|---|---|

| Annual Return | 1.5 – 3% | 3 – 5% | 4 – 6% | Variable (historically high) |

| Risk | Very low | Low to moderate | Moderate | High |

| Liquidity | Immediate | Variable (secondary market) | Low (3-6 months) | Very high (24/7) |

| Recommended Horizon | Short-term | Medium-term (2-5 yrs) | Long-term (8+ yrs) | Medium to long (3+ yrs) |

| Market Correlation | None | Inverse (rates) | Low | Low to moderate |

Conclusion

Corporate treasury investment in crypto assets is no longer a fringe initiative reserved for early tech adopters. With a structured European regulatory framework (MiCA), evolving accounting standards (FASB fair value), and world-class companies validating this approach, the question for a business leader is no longer “why?” but “how?”. The key lies in a methodical approach: define a prudent allocation, choose a regulated platform with corporate-grade support, and integrate this new asset class into a diversified treasury strategy. With the right tools and framework, crypto treasury becomes a coherent performance lever aligned with professional financial management standards.📚 Glossary

- Corporate Treasury : The total cash, liquid assets, and short-term investments available to a company for funding operations and strategic investments.

- CASP (Crypto-Asset Service Provider) : Regulatory status under MiCA requiring authorization to provide crypto services in the EU. Replaces national frameworks like France’s PSAN.

- Fund Segregation : The obligation for a service provider to keep client assets separate from its own funds, ensuring their return in case of insolvency.

- Intangible Asset : Accounting classification for crypto assets under most frameworks (IAS 38, PCG 205x), as they are identifiable assets without physical substance.

- Corporate Tax : Tax levied on business profits. Crypto capital gains are integrated into the taxable result (25% in France, variable rates internationally).

- Fair Value Accounting : Under FASB ASU 2023-08, crypto assets must be measured at fair value each reporting period, with changes recognized in earnings.

- DCA (Dollar Cost Averaging) : Investment strategy of purchasing a fixed amount at regular intervals, regardless of price, to smooth the average acquisition cost.

- Stablecoin : A crypto asset whose value is pegged to a fiat currency (euro, dollar). Examples: USDC, EURC. Allows crypto exposure without price volatility.

Frequently Asked Questions

What percentage of treasury can a company invest in crypto?

Most experts recommend allocating between 3% and 10% of surplus treasury (excluding working capital needs). This range captures the upside potential without compromising the company’s financial stability or liquidity position.

How are crypto gains taxed for corporations?

In most jurisdictions, crypto capital gains are integrated into the corporate tax base. In France, they’re subject to the standard 25% corporate tax rate. In the US, they’re treated as property with capital gains taxation. MiCA does not harmonize tax treatment across the EU.

Is a licensed platform required for corporate crypto investment?

Yes. In Europe, MiCA requires that crypto-asset service providers (CASPs) obtain authorization. In France, PSAN registration with the AMF is mandatory, transitioning to MiCA licensing by July 2026. Using an unlicensed platform exposes the company to legal and counterparty risk.

How should a company account for crypto assets on its balance sheet?

Under FASB (US GAAP), crypto assets must be measured at fair value with changes in earnings (ASU 2023-08). Under IFRS and French GAAP, they’re classified as intangible assets with impairment-only measurement — losses are provisioned but gains are only recognized upon disposal.

Which crypto assets are most suitable for corporate treasury?

Bitcoin (BTC) is the primary choice due to its institutional adoption, liquidity, and track record. Ethereum (ETH) can complement the allocation. Stablecoins (USDC, EURC) provide a non-volatile position within the crypto ecosystem, useful for tactical positioning.

What are the main risks of corporate crypto investment?

Key risks include balance sheet volatility from impairment or fair value changes, reputational risk depending on industry, cybersecurity threats related to custody, and evolving regulatory requirements. A measured allocation combined with a regulated custodian significantly mitigates these risks.

📰 Sources

This article is based on the following sources:

- AMF – MiCA Transition for CASPs

- FASB ASU 2023-08 – Crypto Asset Accounting

- Bitcoin Treasuries

- Skadden – Cryptoasset Treasury Strategies in Public Markets

- Reuters – Crypto-Asset Treasury Strategies

Comment citer cet article : Fibo Crypto. (2026). Corporate Treasury and Crypto: How to Invest Wisely in 2026. Consulté le 24 March 2026 sur https://fibo-crypto.fr/en/blog/invest-corporate-treasury-wisely-cryptocurrency/

The simplest way to buy, swap and manage your crypto

Join the first users and get priority access. No seed phrase, fees 3.5x lower, built-in DeFi yield.

Get early access →