Best Crypto Yield 2026: Complete Comparison of Staking, Lending and DeFi

📋 En bref (TL;DR)

- Ethereum staking yields around 3-4% APY, while Solana reaches 7-8% APY with moderate risk.

- DeFi lending via Aave generates 2-5% APY on stablecoins, transparently and non-custodially.

- Liquid staking (Lido, Jito) combines staking rewards with liquidity — you remain free to use your funds.

- Restaking (EigenLayer) offers additional yields of 5-15% APY, but with significantly higher risk.

- Tokenized RWAs (Ondo, Centrifuge) offer 4-8% APY backed by real-world assets like Treasury bonds.

- CeFi (Binance, Coinbase) is easy to access but requires handing over custody of your funds to a third party.

- Any yield above 20% APY sustained over time is a major red flag — remember Terra/Luna.

- Diversifying across 2-3 audited protocols is the safest strategy for generating yield.

- Crypto yield is taxable — in the US, staking and lending rewards are taxed as income; in the EU, tax treatment varies by country (e.g., France’s 30% flat tax, Germany’s 1-year exemption).

- A non-custodial wallet is essential for maintaining control of your funds while accessing DeFi yields.

Crypto yield in 2026: a more mature market

The crypto yield market in 2026 is structured around 6 major categories — CeFi, DeFi lending, staking, liquid staking, restaking and RWA — with yield levels ranging from 1% to 15% APY depending on the risk taken. After the scandals of 2022 (Terra/Luna, Celsius, FTX, BlockFi), the ecosystem has fundamentally evolved. Triple-digit yield promises have given way to more realistic rates, backed by transparent economic mechanisms.

2026 marks a turning point for several reasons. The MiCA regulation in Europe now imposes strict transparency rules on crypto service providers. The surviving DeFi protocols — Aave, Lido, Compound — have proven their resilience after more than three years of continuous operation without major incidents. Institutional adoption, driven by Bitcoin and Ethereum spot ETFs, has injected billions of dollars of liquidity into the ecosystem.

The fundamental distinction to understand before choosing a yield strategy is the one between CeFi and DeFi, and more precisely between custodial and non-custodial. In CeFi, you entrust your funds to an intermediary (an exchange like Binance or Coinbase) that earns yield on your behalf. In DeFi, your funds remain under your control through a non-custodial wallet, interacting directly with audited smart contracts. The lesson from FTX is clear: custody is the risk.

This guide compares every yield method available as of March 2026 in detail: how it works, real rates, risks, and which investor profile it suits. The goal is to help you build a yield strategy tailored to your risk tolerance, with full knowledge of the trade-offs.

Complete comparison: all yield options in 2026

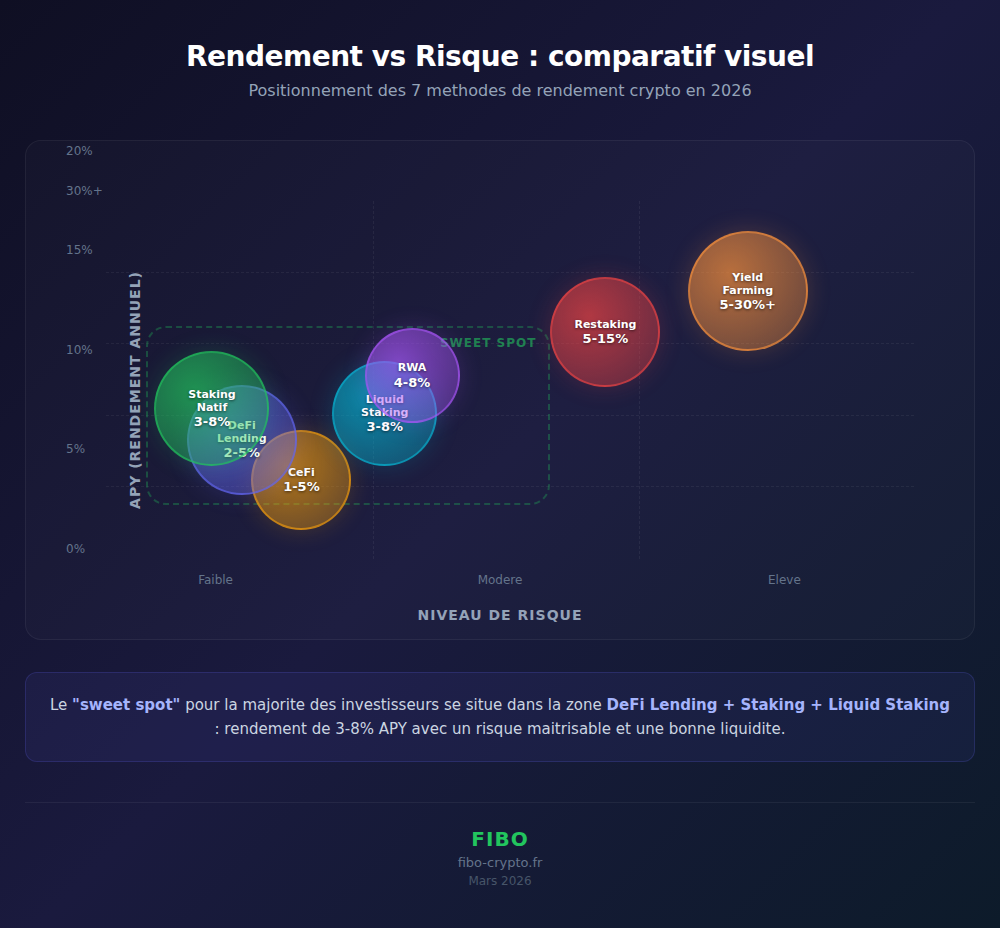

The 7 major crypto yield methods in 2026 offer APYs ranging from 1% (conservative CeFi) to over 30% (aggressive yield farming), with proportional risk levels. The table below summarizes all options available to an investor as of March 2026.

| Method | Typical APY | Risk | Custody | Liquidity | Example |

|---|---|---|---|---|---|

| CeFi (Binance Earn) | 1-5% | Medium | Custodial | High | Binance, Coinbase, Kraken |

| DeFi Lending (Aave) | 2-5% | Low-Medium | Non-custodial | High | Aave, Morpho, Compound |

| Native Staking (ETH) | 3-4% | Low | Variable | Low (unbonding) | Ethereum, Solana, Cardano |

| Liquid Staking | 3-8% | Medium | Non-custodial | High | Lido (stETH), Jito (JitoSOL) |

| Restaking | 5-15% | High | Non-custodial | Medium | EigenLayer, Symbiotic |

| Tokenized RWA | 4-8% | Medium | Variable | Medium | Ondo (OUSG), Centrifuge |

| Yield Farming LP | 5-30%+ | High | Non-custodial | Variable | Curve, Uniswap, Aerodrome |

Several key insights emerge from this comparison. First, there is no high yield without risk. Methods offering over 10% APY (restaking, yield farming) systematically come with high risk — increased smart contract complexity, risk of impermanent loss, or exposure to newer, less battle-tested protocols.

Second, custody is a deciding factor. CeFi solutions are the easiest to use, but they require handing your funds over to a third party. DeFi solutions let you maintain full control through a non-custodial wallet, at the cost of a steeper learning curve.

Third, the “sweet spot” for most investors lies in the DeFi lending + liquid staking zone, which combines yields of 3 to 8% APY with a manageable risk level and decent liquidity.

CeFi: easy yield, but at what cost?

CeFi (centralized finance) yield is the simplest way to earn interest on your crypto — you deposit your assets on an exchange like Binance or Coinbase, and the platform pays you 1 to 5% APY in interest. But this simplicity comes with a hidden cost: you give up full control of your funds.

How it works

The mechanism is similar to a traditional savings account. You deposit your crypto on a centralized platform (Binance Earn, Coinbase Earn, Kraken Staking). The platform then puts your funds to work — lending them to other users, staking them, or deploying them in DeFi protocols for its own account. In return, it passes on a portion of the profits as interest.

Rates as of March 2026 are as follows: Binance Earn offers 1-3% APY on Bitcoin, 2-4% on Ethereum, and up to 5% on stablecoins (USDT, USDC). Coinbase offers slightly lower rates but with a more beginner-friendly interface. Kraken sits between the two, with a strong security track record.

Binance Earn: 1-5% APY | Coinbase Earn: 1-4% APY | Kraken Staking: 2-5% APY | Advantage: maximum simplicity | Drawback: custody handed over to a third party

The problem: custody

The major risk of CeFi can be summed up in three letters: FTX. In November 2022, the exchange FTX — then the world’s second-largest — collapsed overnight, resulting in the loss of over $8 billion in customer funds. Users who had deposited their crypto on the platform to earn yield lost everything. Celsius, BlockFi and Voyager Digital followed the same path.

The fundamental problem is structural: when you deposit your crypto on an exchange, it’s no longer your crypto. Legally, you become a creditor of the company. If it goes bankrupt, misuses your funds, or gets hacked, you have no guarantee of recovering your assets. The saying “Not your keys, not your coins” isn’t a cliche — it’s a legal reality.

CeFi verdict

CeFi remains relevant for absolute beginners who want to explore crypto yield with a limited amount. Depositing the equivalent of $100 to $500 on Binance Earn to understand the mechanics is reasonable. However, entrusting a significant share of your crypto portfolio to a centralized intermediary is a risk that the events of 2022 made unacceptable for any informed investor. The transition to non-custodial solutions (DeFi lending, staking) should be the next step.

DeFi Lending: Aave, Morpho, Compound — transparent yield

DeFi lending lets you lend your crypto through audited smart contracts, without intermediaries, and earn 2 to 5% APY on stablecoins — all while retaining control of your funds from your non-custodial wallet. It’s the yield method that offers the best balance between security, transparency and returns in 2026.

The mechanism is elegant in its simplicity: you deposit your crypto (stablecoins, ETH, wBTC) into a lending protocol. These funds are made available to borrowers, who must deposit collateral worth more than the amount borrowed (over-collateralization). Interest rates adjust automatically based on supply and demand. No human intervenes — everything is managed by code.

Aave: the undisputed leader

Aave is the world’s number one DeFi lending protocol, with a TVL (Total Value Locked) exceeding $40 billion as of March 2026. Present on more than 10 blockchains (Ethereum, Arbitrum, Base, Polygon, Optimism, Avalanche), Aave has processed billions of dollars in loans without a major incident since its launch in 2020.

Aave lending rates as of March 2026 sit around 3-5% APY on stablecoins (USDC, USDT, DAI), 1-2% APY on ETH, and variable rates on other assets. Version V4, currently being deployed, introduces a “unified liquidity layer” that optimizes capital efficiency and improves rates for depositors.

The native stablecoin GHO, issued by Aave, adds an additional dimension to the ecosystem. Borrowers can use GHO at preferential rates, while stkAAVE (staked AAVE) holders benefit from discounts on borrowing fees.

Morpho: the rate optimizer

Morpho takes an innovative approach by combining the best of lending pools (Aave/Compound) with peer-to-peer matching. When a lender and a borrower can be matched directly, Morpho eliminates the pool spread and offers better rates to both parties. As of March 2026, Morpho manages several billion dollars in TVL and regularly offers rates 0.5 to 1 point above Aave on certain assets.

Compound: the veteran

Compound, launched in 2018, is the protocol that popularized the DeFi lending concept. Its algorithmic rates adjust in real time based on pool utilization. While its market share has declined against Aave, Compound remains a reliable protocol with a proven security track record and billions of dollars in TVL.

Aave V3/V4: 3-5% APY stablecoins | Morpho: 3.5-6% APY (P2P matching) | Compound V3: 2-4% APY stablecoins | All non-custodial, all audited, combined TVL: $50B+

The main risk of DeFi lending is smart contract risk — a bug or vulnerability in the code could lead to loss of funds. This is why it’s essential to favor protocols that have undergone multiple security audits by recognized firms (Trail of Bits, OpenZeppelin, Certora) and have managed billions of dollars for several years without incident. Aave, Morpho and Compound meet these criteria.

Staking: the “healthiest” yield in the ecosystem

Staking involves locking up your crypto to secure a Proof-of-Stake blockchain network, in exchange for regular rewards — it’s the most fundamental and economically “clean” yield mechanism, because it compensates a real service: securing the network. Unlike lending or yield farming, staking yield comes directly from the protocol’s inflation and transaction fees, not from a borrower.

Ethereum: maximum security, modest yield

Ethereum staking offers a yield of approximately 3.2% APY as of March 2026 — a modest rate but backed by the most secure and decentralized blockchain after Bitcoin. ETH staking contributes to securing a network that hosts more than 75% of global DeFi value.

Solo staking (running your own validator) requires a minimum deposit of 32 ETH (approximately $80,000 at current prices) and the technical expertise to maintain a node online 24/7. For most investors, delegated staking or staking pools are the most accessible alternatives. Slashing penalties (reduction of stake for malicious validator behavior) exist but remain rare on established validators.

The main drawback of native ETH staking is the unbonding period — the time required to withdraw your funds after you stop staking. Since the Shanghai upgrade, withdrawals are possible but subject to a queue that can take several days during high-demand periods.

Solana: more attractive rates

Solana offers a significantly higher staking yield, around 7-8% APY, with no minimum staking requirement and simple delegation to a validator from any compatible wallet. SOL inflation is currently around 5.5%, with a progressive reduction mechanism (disinflationary).

Solana staking is particularly accessible: no minimum, delegation in a few clicks from Phantom or another wallet, and short unbonding periods (approximately 2-3 days). Solana validators number in the thousands, providing a good level of decentralization.

Ethereum: ~3.2% APY (32 ETH min solo) | Solana: ~7-8% APY (no minimum) | Cardano: ~3% APY | Polkadot: ~14% APY | Cosmos: ~15-20% APY | Note: a high APY may reflect high inflation

Other PoS chains: Cardano, Polkadot, Cosmos

Cardano (ADA) offers approximately 3% APY with simple staking and no lock-up period — your ADA remains liquid while staking. It’s one of the most user-friendly staking systems on the market. Polkadot (DOT) offers higher yields around 14% APY, but with significant inflation and a more complex validator nomination mechanism. Cosmos (ATOM) shows the highest rates in the segment, at 15-20% APY, but with proportionally high token inflation.

A crucial point: a high APY does not automatically mean high real yield. If a token offers 20% staking APY but its annual inflation is 15%, the real net yield is only 5% — and that’s without accounting for the potential depreciation of the token against the dollar.

Staking risks

Staking is generally considered the safest yield method in crypto, but it still carries risks. Slashing can lead to partial loss of your staked funds if the chosen validator acts maliciously or stays offline for too long. The unbonding period makes your funds illiquid for several days to several weeks depending on the blockchain. Finally, the risk of depreciation of the underlying token remains — 8% APY doesn’t compensate for a 50% price drop.

Liquid staking and restaking: a double-edged innovation

Liquid staking solves the main drawback of traditional staking — your funds being illiquid — by issuing you a liquidity token (stETH, JitoSOL, rETH) that you can use freely in DeFi while still receiving staking rewards. Restaking, a more recent innovation, lets you reuse those same staked funds to secure additional protocols and generate extra yield.

Liquid staking — Lido, Jito, Rocket Pool

Lido is the undisputed leader in liquid staking with over $30 billion in TVL. When you deposit ETH on Lido, you receive stETH — a token that represents your staked ETH plus accumulated rewards. stETH can be used in other DeFi protocols (Aave, Curve, Uniswap) to generate additional yield. The base rate is approximately 3.5% APY, equivalent to native ETH staking, but with immediate liquidity.

Jito is the equivalent on Solana. By depositing SOL, you receive JitoSOL, which generates approximately 7.5% APY while remaining usable within the Solana DeFi ecosystem. Jito adds a MEV (Maximal Extractable Value) mechanism that captures additional value for stakers.

Rocket Pool stands out for its decentralization — unlike Lido, which concentrates a significant share of ETH staking, Rocket Pool distributes staking across a large number of independent node operators. Its rETH token is considered the most decentralized in the segment, with an APY comparable to Lido.

Restaking — EigenLayer and shared security

Restaking, popularized by EigenLayer, is the most significant innovation in crypto yield in 2025-2026. The concept: reuse ETH that is already staked (via Lido or natively) to simultaneously secure other protocols — oracles, bridges, rollups. In exchange for this additional security, restakers receive extra rewards.

Restaking yields sit between 5 and 15% APY in total (base staking + restaking rewards), depending on the protocols being secured. EigenLayer has accumulated over $15 billion in TVL, making it one of the fastest-growing protocols in DeFi history. Symbiotic, a competitor to EigenLayer, offers a similar approach with slightly different mechanics.

The risks: layers of complexity

The innovation of liquid staking and restaking comes with additional risks. Each added layer (native staking, liquid staking, restaking) introduces a new smart contract risk. A bug in the restaking protocol could lead to loss of funds, regardless of the security of the underlying staking.

The risk of de-pegging is also present: if stETH or JitoSOL decouples from the value of the underlying asset (as briefly happened in 2022 during the Terra crisis), holders suffer a loss. The complexity of restaking (ETH staked on Lido, stETH deposited on EigenLayer, then used as collateral on Aave) creates chains of dependency where a problem at any link can cascade.

The rule of caution is simple: never invest in a restaking protocol more than you can afford to lose, and limit your exposure to this category to a maximum of 10-20% of your yield allocation.

RWA: tokenized real-world assets

Tokenized RWAs (Real World Assets) offer yield backed by tangible assets — U.S. Treasury bonds, real estate, private credit — via the blockchain, with rates of 4 to 8% APY and a very different risk profile from other crypto categories. It’s the most concrete convergence between traditional finance and DeFi.

Ondo Finance is the segment leader with its OUSG (Ondo US Government Bond) token, backed by short-term U.S. Treasury bonds. The yield tracks the federal funds rate — around 5% APY as of March 2026 — with near-zero credit risk since it’s tokenized U.S. sovereign debt. Ondo has surpassed $1 billion in TVL.

Centrifuge tokenizes private receivables (invoices, real estate loans, commercial credit) and makes them accessible to DeFi investors. Yields are higher (6-8% APY) but credit risk is also greater. Maple Finance specializes in uncollateralized institutional loans, offering attractive rates but with real default risk.

Tokenized RWAs represent a particularly interesting opportunity for investors seeking yields above traditional savings accounts, backed by assets they understand (government bonds, real estate), while benefiting from the transparency and composability of blockchain. The main risk remains dependence on the token issuer and the legal framework linking the tokenized asset to the real asset.

Red flags: when the yield is too good to be true

Any crypto yield above 20% APY sustained over time should be considered suspicious until proven otherwise — recent crypto history is littered with projects offering sky-high yields that turned out to be disguised Ponzi schemes. Knowing how to spot these red flags is just as important as knowing where to invest.

The most emblematic case remains Terra/Luna and its UST stablecoin, which promised a 20% APY yield via the Anchor protocol. In May 2022, the UST collapse wiped out more than $40 billion in market cap within days. Hundreds of thousands of investors lost all their funds. The yield actually came from finite reserves that were inexorably depleting — an unsustainable scheme by definition.

Celsius and BlockFi offered rates of 8 to 17% APY on crypto deposits. Behind these attractive rates lay disastrous risk management: uncollateralized loans to risky counterparties, investments in opaque DeFi protocols, and a business model where losses were covered by deposits from new users.

Here are the red flags to watch for systematically:

- APY above 20% with no clear explanation of where the yield comes from

- Anonymous or pseudo-anonymous team with no verifiable track record

- No security audit by a recognized firm (Trail of Bits, OpenZeppelin, Certora)

- Explosive TVL growth with no real underlying product — a sign of a Ponzi scheme

- “Guaranteed” yield — no yield is guaranteed in crypto, ever

- Circular mechanism: the yield comes from the token itself (token printing)

- Pressure to invest quickly (“APY dropping soon”, “limited spots”)

The question to always ask: “Where does the yield come from?” In staking, it comes from protocol inflation and fees. In lending, it comes from interest paid by borrowers. In yield farming, it comes from trading fees. If the answer is vague or circular, walk away.

Which strategy for which profile?

The best crypto yield strategy depends on your risk tolerance, your experience with DeFi and the amount you want to allocate — a cautious beginner and an experienced investor don’t have the same needs. Here are three typical profiles with tailored allocations.

| Profile | Allocation | Expected yield | Methods |

|---|---|---|---|

| Conservative | Stablecoins + blue chips | 3-5% APY | CeFi (small amount) + ETH staking + Aave stablecoin lending |

| Moderate | Mix stablecoins + ETH/SOL | 5-8% APY | Aave lending + liquid staking (Lido/Jito) + RWA (Ondo) |

| Aggressive | Diversified multi-asset | 8-15% APY | Liquid staking + restaking (EigenLayer) + LP (Curve) + RWA |

Conservative profile (beginner or risk-averse): The goal is to beat traditional savings account yields (e.g., ~4.5% for US high-yield savings, ~3% for EU regulated accounts) while minimizing risk. The allocation relies on native ETH staking (~3.2% APY), stablecoin lending on Aave (~3-5% APY), and optionally a small amount in CeFi for simplicity. The overall target yield is 3-5% APY with low risk. Spread across 2 protocols maximum.

Moderate profile (informed investor): You understand the basics of DeFi and are comfortable using a non-custodial wallet. The allocation combines liquid staking (Lido stETH or Jito JitoSOL for 3.5-8% APY), lending on Aave or Morpho (~3-6% APY), and exposure to RWAs (Ondo OUSG for ~5% APY). The overall target yield is 5-8% APY. Diversify across 2-3 protocols.

Aggressive profile (DeFi expert): You understand advanced mechanisms and accept high risk for higher yields. The allocation includes restaking via EigenLayer (5-15% APY), liquidity provision on Curve or Aerodrome (10-30% APY with risk of impermanent loss), and composed strategies (stETH as collateral on Aave). The overall target yield is 8-15% APY, but complexity and risk are proportional. Do not exceed 3-4 protocols simultaneously.

Regardless of your strategy, a non-custodial wallet is the essential foundation. It’s what lets you maintain control of your funds while accessing DeFi protocols. Next-generation wallets, with built-in DeFi access and simplified key management, eliminate the technical complexity that used to hinder adoption.

Conclusion: smart yield in 2026

Crypto yield in 2026 is no longer an opaque jungle where scams sit alongside opportunities — it’s a structured ecosystem, with battle-tested protocols, rigorous security audits, and realistic yields that reflect actual risk.

Three principles sum up a healthy approach to crypto yield. First, understand where the yield comes from before investing — staking (network security), lending (borrower interest), LP (trading fees). If the source is unclear, the risk is maximum. Second, diversify across 2-3 audited protocols rather than concentrating everything on a single yield source. Third, use a non-custodial wallet to keep control of your funds — the lessons of FTX, Celsius and BlockFi must never be forgotten.

The integration between non-custodial wallets and DeFi protocols is the most significant shift of 2026. Solutions like Fibo, which integrate Aave lending directly into the wallet, allow anyone to earn yield on their stablecoins in a few taps — without compromising the security of their funds. It’s this combination of simplicity and self-sovereignty that finally makes crypto yield accessible to everyone.

Start small, learn, then gradually increase your exposure. The best yield is the one you understand.

Glossary

- APY (Annual Percentage Yield): The annual rate of return including compound interest. Unlike APR, APY accounts for the automatic reinvestment of gains. An APY of 5% means $1,000 invested generates $50 in yield per year.

- APR (Annual Percentage Rate): The simple annual interest rate, without compound interest. APR is always less than or equal to APY for the same investment. Some DeFi protocols display APR, others APY — always check which one is being used.

- Staking: A mechanism that involves locking up cryptocurrencies to participate in transaction validation on a Proof-of-Stake blockchain, in exchange for regular rewards in the form of additional tokens.

- Liquid Staking: A variant of staking that issues a liquidity token (stETH, JitoSOL, rETH) representing the staked funds. This token remains usable in DeFi, solving the illiquidity problem of traditional staking.

- Restaking: An innovation that allows already-staked assets to be reused to simultaneously secure other protocols (oracles, bridges, rollups), generating additional rewards. Popularized by EigenLayer on Ethereum.

- DeFi (Decentralized Finance): A set of financial services (lending, borrowing, trading, insurance) operating on blockchain via smart contracts, without banking intermediaries or trusted third parties.

- Lending: In DeFi, lending allows you to lend your cryptocurrencies via a decentralized protocol (Aave, Compound, Morpho) and receive interest paid by borrowers. Funds remain under the control of audited smart contracts.

- Yield Farming: A strategy that involves moving funds between different DeFi protocols to maximize returns. Includes providing liquidity in trading pools (LP), farming governance tokens, and composed strategies.

- TVL (Total Value Locked): The total value of assets deposited in a DeFi protocol. It’s the primary metric for measuring adoption and user confidence. A high and stable TVL is a positive signal.

- Smart Contract: A self-executing computer program deployed on a blockchain. It automatically executes the terms of an agreement (loan, exchange, staking) when predefined conditions are met, without human intervention.

- Slashing: A penalty applied to a validator that acts maliciously or stays offline for too long. A portion of their staked funds is confiscated. This mechanism incentivizes validators to maintain correct behavior.

- Impermanent Loss: A loss incurred by liquidity providers in a trading pool when the price of deposited assets diverges from the time of deposit. The greater the divergence, the larger the loss. It becomes “permanent” if you withdraw your funds.

- Custody: Refers to who holds control of the private keys associated with cryptocurrencies. In traditional custody (CeFi), a third party (exchange, bank) holds your keys. The risk: if that third party goes bankrupt (FTX), your funds are lost.

- Non-custodial (Self-custody): A management mode where the user retains exclusive control of their private keys through a personal wallet. No third party can access, freeze, or seize the funds. It’s the recommended standard for security in crypto.

- RWA (Real World Assets): Real-world assets (Treasury bonds, real estate, private credit, commodities) tokenized on the blockchain. Allows earning yield backed by tangible assets via DeFi rails.

- Stablecoin: A cryptocurrency whose value is pegged to a stable asset, typically the US dollar (USDC, USDT, DAI). Used as a store of value and medium of exchange in DeFi without being exposed to the volatility of other cryptos.

- Unbonding: The waiting period required to withdraw your funds after you stop staking. The duration varies by blockchain: a few days on Solana, up to several weeks on some chains. During this period, funds are illiquid.

- Protocol: A set of rules and smart contracts that define how a DeFi service operates (Aave for lending, Lido for liquid staking, Uniswap for trading). A protocol is typically governed by its community via a governance token.

Frequently Asked Questions

What is the best crypto yield in 2026?

The best crypto yield in 2026 depends on your risk profile. For a safe and transparent return, DeFi lending via Aave offers 3-5% APY on stablecoins in a non-custodial setup. Solana staking reaches 7-8% APY. Liquid staking (Lido, Jito) combines yield and liquidity. For the more adventurous, restaking via EigenLayer can reach 5-15% APY, but with proportional risk. The sweet spot for most investors lies between 5 and 8% APY via a combination of lending + liquid staking.

Is crypto staking profitable?

Yes, staking is profitable in 2026, provided you account for token inflation and volatility. Ethereum staking offers around 3.2% APY — modest but backed by the most secure blockchain. Solana staking earns 7-8% APY with more risk. Real profitability depends on the token’s price movement: 8% APY doesn’t offset a 30% price drop. To minimize this risk, stablecoin lending via Aave offers 3-5% APY without volatility exposure.

What is the Ethereum staking yield?

Ethereum staking offers approximately 3.2% APY as of March 2026. Solo staking requires a minimum of 32 ETH (approximately $80,000). For smaller amounts, liquid staking via Lido (stETH) or Rocket Pool (rETH) offers an equivalent yield with no minimum, plus the advantage of keeping your funds liquid. Rewards come from ETH protocol inflation and transaction fees.

How to earn interest on crypto?

There are 6 main methods: 1) Native staking (ETH, SOL) for 3-8% APY. 2) DeFi lending via Aave or Compound for 2-5% APY. 3) Liquid staking via Lido or Jito to combine yield and liquidity. 4) CeFi (Binance Earn) for simplicity, but you give up custody. 5) Tokenized RWAs (Ondo) for yield backed by real-world assets. 6) Yield farming for experts. Favor a non-custodial wallet to maintain control of your funds.

Is yield farming risky?

Yes, yield farming is the riskiest crypto yield method. The main risks are: impermanent loss (loss due to price divergence), smart contract risk (bugs or exploits), and volatility of reward tokens. Displayed APYs of 20-100% are often temporary. Advanced yield farming is reserved for DeFi experts. For other investors, lending (Aave) and staking offer more modest but significantly safer returns.

What is the difference between staking and lending?

Staking involves locking up your crypto to secure a blockchain network — the yield comes from protocol inflation and fees. Lending involves lending your crypto to borrowers via a DeFi protocol — the yield comes from interest paid. Key difference: staking exposes you to the volatility of the token, while stablecoin lending offers yield without volatility. Both are compatible in a diversified strategy.

Should I use CeFi or DeFi for yield?

DeFi is preferred for crypto yield in 2026, because it lets you keep control of your funds (non-custodial). The failures of FTX, Celsius and BlockFi demonstrated the risk of CeFi. DeFi via audited protocols like Aave offers comparable yields (3-5% APY) with full transparency. CeFi remains relevant for beginners with small amounts, but transitioning to DeFi should be the medium-term goal.

What is liquid staking?

Liquid staking solves the illiquidity problem of traditional staking. When you stake ETH via Lido, you receive stETH — a token that represents your staked ETH plus accumulated rewards. This stETH can be used in other DeFi protocols (Aave, Curve) to generate additional yield, while you continue earning staking rewards (~3.5% APY). The main protocols are Lido (stETH), Rocket Pool (rETH) and Jito (JitoSOL).

How to avoid crypto yield scams?

Follow these rules: 1) Be suspicious of any APY above 20% sustained over time. 2) Verify that the protocol has been audited by recognized firms (Trail of Bits, OpenZeppelin). 3) Ask yourself where the yield comes from. 4) Avoid anonymous teams with no track record. 5) Favor protocols with over a year of history and billions in TVL. 6) Never entrust all your funds to a single protocol.

Is crypto staking and lending income taxable?

Yes, crypto staking and lending income is taxable in most jurisdictions. In the US, staking rewards are typically taxed as ordinary income at the time of receipt, and capital gains tax applies upon disposal. In the EU, treatment varies: France applies a 30% flat tax on realized crypto gains, Germany exempts holdings held over 1 year, and other countries have their own rules. It’s essential to keep records of all transactions. Tools like CoinTracker, Koinly, or CoinTracking help with tax reporting.

Sources

This article relies on the following sources:

- DefiLlama — TVL (Total Value Locked) data for all DeFi protocols, including Aave, Lido, EigenLayer and Compound.

- Aave — Protocol documentation — Official Aave lending protocol documentation, including V3/V4 specifications and yield rates.

- Lido Finance — Staking statistics — Ethereum staking statistics, stETH yields and liquid staking protocol data.

- EigenLayer — Restaking documentation — Technical documentation for the EigenLayer restaking protocol, shared security mechanisms and yields.

- CoinGecko — Staking APY data — Staking yield data for all Proof-of-Stake blockchains.

- Ethereum.org — Staking rewards — Official Ethereum staking guide, yields, participation requirements and risks.

- Solana — Validator economics — Official documentation on Solana validator economics, staking rates and inflation mechanisms.

- Ondo Finance — RWA documentation — Ondo Finance protocol documentation, Treasury bond tokenization and RWA yields.

- SEC — Crypto regulation — U.S. regulatory framework for crypto assets and digital securities.

- European Commission — MiCA Regulation — European regulatory framework for crypto-asset markets (Markets in Crypto-Assets).

How to cite this article: Fibo Crypto. (2026). Best Crypto Yield 2026: Complete Comparison of Staking, Lending and DeFi. Retrieved from https://fibo-crypto.fr/en/blog/best-crypto-yield-2026-complete-comparison-of-all-options

The simplest way to buy, swap and manage your crypto

Join the first users and get priority access. No seed phrase, fees 3.5x lower, built-in DeFi yield.

Get early access →