How Does Blockchain Work? Complete Guide to Blockchain Technology [2026]

📋 En bref (TL;DR)

- Blockchain is a distributed ledger technology that records data across multiple computers, making information transparent, secure, and virtually impossible to alter

- Blocks contain transaction data linked together using cryptographic hash functions, creating an immutable chain of records

- Decentralization eliminates intermediaries: No single entity controls the network; thousands of nodes maintain identical copies of the data

- Consensus mechanisms like Proof of Work and Proof of Stake allow networks to agree on valid transactions without trusted third parties

- Cryptographic hashing ensures security: Any change to data would alter the hash, immediately alerting the network to tampering attempts

- Immutability guarantees data integrity: Once recorded, transactions cannot be modified or deleted, creating a permanent audit trail

- Applications extend far beyond cryptocurrency: Blockchain transforms supply chains, healthcare, voting systems, digital identity, and financial services worldwide

Blockchain technology has fundamentally changed how we think about digital transactions, data security, and trust in the digital age. Since the launch of Bitcoin in 2009, this revolutionary technology has grown from an obscure concept among cryptographers to a transformative force affecting industries worldwide. But how does blockchain actually work?

In this comprehensive guide, we’ll break down blockchain technology into understandable components. You’ll learn how blocks are created, why decentralization matters, and how cryptographic hash functions secure the entire system. Whether you’re a complete beginner or looking to deepen your understanding, this guide covers everything you need to know about how blockchain works.

What Is Blockchain Technology?

Definition: A Distributed Digital Ledger

At its core, blockchain is a distributed ledger technology (DLT) that records information across a network of computers. Unlike traditional databases controlled by a single entity, blockchain spreads data across thousands of nodes, with each maintaining an identical copy of the entire transaction history.

Think of blockchain as a shared Google spreadsheet that thousands of people can view simultaneously, but with one crucial difference: once data is entered, it cannot be edited or deleted. Every change creates a new entry while preserving the complete history of all previous records.

The name “blockchain” describes exactly how the technology works: data is grouped into blocks, and these blocks are chained together in chronological order using cryptographic techniques. This simple yet powerful architecture creates a tamper-proof record of all transactions.

Key Characteristics of Blockchain

What makes blockchain revolutionary isn’t any single feature, but the combination of several characteristics working together:

- Decentralization: No central authority or single point of failure. The network operates through consensus among participants.

- Transparency: All transactions are visible to network participants, enabling verification without trust.

- Immutability: Once recorded, data cannot be altered without changing all subsequent blocks, which is computationally infeasible on large networks.

- Security: Advanced cryptography protects data and ensures only authorized parties can initiate transactions.

- Programmability: Many blockchains support smart contracts—self-executing code that automates agreements.

Brief History: From Bitcoin to Today

The concept of blockchain was first described in 1991 by Stuart Haber and W. Scott Stornetta, who proposed a cryptographically secured chain of blocks for timestamping digital documents. However, blockchain technology remained largely theoretical until 2008, when an anonymous person or group using the pseudonym Satoshi Nakamoto published the Bitcoin whitepaper.

Bitcoin launched in January 2009 as the first practical application of blockchain technology. In 2015, Ethereum introduced smart contracts, dramatically expanding what blockchains could do. Today, thousands of blockchain projects exist, from decentralized finance (DeFi) applications to supply chain management systems used by Fortune 500 companies.

How Does Blockchain Work? The Complete Transaction Process

Understanding how blockchain works requires following a transaction from initiation to final confirmation. Let’s trace the complete journey of a typical blockchain transaction.

Step 1: Transaction Initiation

Every blockchain transaction begins when a user initiates a transfer. In cryptocurrency networks, User A wants to send digital assets to User B. Using a crypto wallet, User A creates a transaction specifying:

- The recipient’s public address (similar to an account number)

- The amount being transferred

- A transaction fee (incentive for validators)

The user signs this transaction with their private key, creating a digital signature that proves ownership of the funds without revealing the key itself. This cryptographic signature is mathematically verifiable by anyone on the network.

Step 2: Broadcasting to the Network

Once signed, the transaction is broadcast to the blockchain network. It propagates from node to node until it reaches thousands of computers worldwide. The transaction enters the mempool (memory pool)—a waiting area where unconfirmed transactions queue for processing.

Transactions in the mempool are visible to miners and validators, who select which ones to include in the next block. Generally, transactions with higher fees get prioritized, as validators earn these fees as part of their reward.

Step 3: Validation and Verification

Nodes across the network independently verify each transaction. They check several conditions:

- Valid signature: Does the digital signature match the sender’s public key?

- Sufficient balance: Does the sender have enough funds to complete the transfer?

- No double-spending: Are these funds being spent only once?

- Correct format: Does the transaction follow network rules?

Transactions that fail any check are rejected. Valid transactions remain in the mempool, waiting to be included in a block.

Step 4: Block Creation

Miners (in Proof of Work systems) or validators (in Proof of Stake systems) gather verified transactions from the mempool and bundle them into a new block. Each block contains:

- A block header with metadata

- A list of transactions (hundreds to thousands)

- The hash of the previous block

- A timestamp

- A nonce (in PoW systems)

In Proof of Work, miners compete to solve a complex mathematical puzzle—finding a nonce that produces a hash below a target difficulty. This process requires enormous computational power but ensures only valid blocks are added.

Step 5: Block Added to the Chain

When a miner solves the puzzle (or a validator is selected in PoS), they broadcast the new block to the network. Other nodes verify the block is valid, then add it to their copy of the blockchain. The winning miner receives:

- Block reward: New cryptocurrency created by the protocol (e.g., 3.125 BTC per block as of 2024)

- Transaction fees: All fees from included transactions

The block is now part of the permanent record. However, one confirmation isn’t considered fully secure.

Step 6: Confirmation

As more blocks are added on top, the transaction gains additional confirmations. Each new block makes altering the transaction exponentially more difficult. Bitcoin transactions are typically considered secure after 6 confirmations (approximately 1 hour), while Ethereum transactions may be considered final more quickly.

After sufficient confirmations, User B can confidently spend the received funds, knowing the transaction is essentially irreversible.

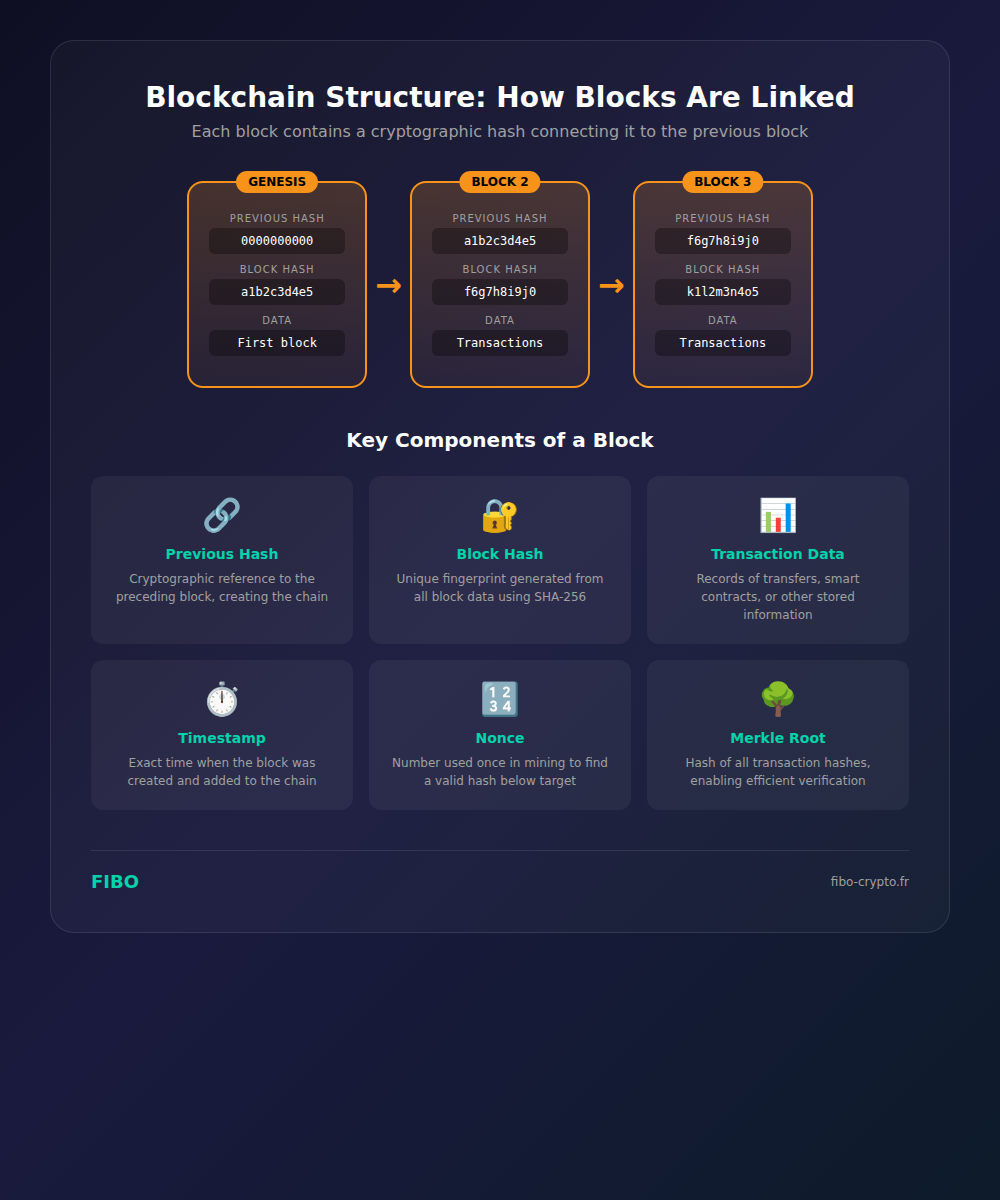

Understanding Blocks and Chains: The Core Architecture

What Is a Block?

A block is the fundamental unit of blockchain data storage. Think of each block as a page in a ledger book—it contains a specific set of records and includes information linking it to the previous page. The structure of a block typically includes:

Block Header (metadata about the block):

- Previous Block Hash: A 256-bit reference to the preceding block, creating the “chain”

- Merkle Root: A single hash representing all transactions in the block

- Timestamp: When the block was created

- Difficulty Target: The mining difficulty when the block was created

- Nonce: The number that solves the proof-of-work puzzle

Block Body (the actual data):

- Transaction Counter: Number of transactions in the block

- Transaction List: All individual transactions

The Genesis Block

Every blockchain begins with a special first block called the Genesis Block (Block 0). This block is hardcoded into the software and serves as the foundation for the entire chain. Bitcoin’s genesis block, mined on January 3, 2009, famously contains the message: “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.”

How Blocks Form a Chain

Each block contains the cryptographic hash of the previous block’s header. This creates an unbreakable link: if anyone tries to modify data in Block 5, it changes Block 5’s hash, which means Block 6’s “previous hash” no longer matches, breaking the chain. This cascading effect makes tampering immediately detectable.

The longer the chain grows, the more secure earlier transactions become. To alter a transaction from 100 blocks ago, an attacker would need to recalculate the proof-of-work for that block AND all 100 subsequent blocks—faster than the entire rest of the network is adding new blocks. On major networks like Bitcoin, this is practically impossible.

Cryptographic Hash Functions: The Security Foundation

What Is a Cryptographic Hash?

A cryptographic hash function is a mathematical algorithm that converts input data of any size into a fixed-length output called a hash (or digest). The most common hash function in blockchain is SHA-256 (Secure Hash Algorithm 256-bit), which produces a 64-character hexadecimal output.

Key properties of cryptographic hash functions:

- Deterministic: The same input always produces the same output

- One-way: You cannot reverse-engineer the original data from the hash

- Collision-resistant: It’s virtually impossible to find two different inputs producing the same hash

- Avalanche effect: A tiny change in input creates a completely different hash

Example of Hashing

Consider these SHA-256 hashes:

- Input: “Hello” → Hash:

185f8db32271fe25f561a6fc938b2e264306ec304eda518007d1764826381969 - Input: “Hello.” → Hash:

5eb67f9f8409b9c3f739735633cbdf92121393d0e13bd0f464b1b2a6a15ad2dc

Adding a single period completely changes the hash—this is the avalanche effect. If someone tried to alter transaction data, the new hash would be obviously different, alerting the network to tampering.

How Hashing Secures Blockchain

Blockchain uses hashing in multiple ways:

- Block linking: Each block’s hash includes the previous block’s hash in its calculation

- Transaction verification: Merkle trees efficiently verify transaction inclusion

- Mining: Proof of Work requires finding a hash below a target value

- Address generation: Wallet addresses derive from public key hashes

Decentralization: Why No Central Authority Controls Blockchain

The Problem with Centralization

Traditional systems rely on central authorities: banks verify transactions, governments issue currencies, companies store data. This creates several vulnerabilities:

- Single point of failure: If the central server goes down, the entire system stops

- Censorship risk: The authority can block transactions or freeze accounts

- Privacy concerns: One entity controls all your data

- Trust requirement: Users must trust the institution to act honestly

How Decentralization Works

Decentralization distributes control across thousands of independent participants. In a decentralized blockchain:

- Every node stores a complete copy of the blockchain

- No single entity can modify records unilaterally

- The network continues functioning even if many nodes go offline

- Rules are enforced by software, not institutions

Bitcoin’s network, for example, includes tens of thousands of full nodes across 100+ countries. To compromise Bitcoin, an attacker would need to simultaneously control the majority of these globally distributed computers—a practically impossible task.

The Role of Nodes

Nodes are computers that participate in the blockchain network. Different types of nodes serve different functions:

- Full Nodes: Store the complete blockchain history and verify all transactions against consensus rules

- Light Nodes: Store only block headers, relying on full nodes for verification

- Mining/Validator Nodes: Participate in creating new blocks (hardware-intensive)

- Archive Nodes: Store complete historical state data (extremely storage-intensive)

Consensus Mechanisms: How the Network Agrees

Without a central authority, how do thousands of computers agree on the valid state of the blockchain? This is the role of consensus mechanisms—protocols that enable distributed agreement.

Proof of Work (PoW)

Proof of Work, introduced by Bitcoin, requires miners to solve computational puzzles to create new blocks. The process:

- Miners collect pending transactions into a block

- They repeatedly hash the block header with different nonce values

- The goal is finding a hash below the network’s difficulty target

- The first miner to find a valid hash broadcasts the block

- Other nodes verify the solution (easy) and add the block to their chain

Advantages: Extremely secure, battle-tested for 15+ years, simple economic incentives

Disadvantages: High energy consumption, expensive hardware requirements, slower transaction speeds

Proof of Stake (PoS)

Proof of Stake selects validators based on the amount of cryptocurrency they “stake” as collateral. Instead of competing through computation, validators are chosen randomly (weighted by stake) to propose blocks.

- Validators lock up tokens as collateral

- The protocol randomly selects a validator to propose the next block

- Other validators attest to the block’s validity

- Validators earn rewards proportional to their stake

- Malicious behavior results in “slashing”—losing staked tokens

Advantages: 99%+ more energy efficient, lower barrier to entry, potentially faster finality

Disadvantages: Less battle-tested, potential centralization around wealthy stakeholders

Ethereum transitioned from Proof of Work to Proof of Stake in September 2022 (called “The Merge”), reducing its energy consumption by approximately 99.95%.

Other Consensus Mechanisms

Delegated Proof of Stake (DPoS): Token holders vote for a small number of delegates who produce blocks. Used by EOS and TRON. Very fast but more centralized.

Proof of Authority (PoA): Pre-approved validators with verified identities create blocks. Used in private/consortium blockchains. Extremely fast but requires trust in validators.

Proof of History (PoH): Solana’s innovation that creates a cryptographic timestamp, enabling parallel transaction processing. Achieves high throughput but with increased complexity.

Types of Blockchain Networks

Public Blockchains

Public blockchains are completely open—anyone can join, view transactions, and participate in consensus. They’re often called “permissionless” because no approval is needed to participate.

Examples: Bitcoin, Ethereum, Cardano, Solana

Characteristics:

- Fully transparent—all transactions visible to anyone

- Truly decentralized—no single controlling entity

- Censorship-resistant—no authority can block transactions

- Native cryptocurrency required for transactions

Private Blockchains

Private blockchains restrict who can participate, read data, and validate transactions. They’re “permissioned” systems where an organization controls access.

Examples: Hyperledger Fabric, R3 Corda

Characteristics:

- Fast and scalable (fewer nodes to achieve consensus)

- Privacy controls—data visible only to authorized participants

- Centrally administered—one organization sets the rules

- No public cryptocurrency needed

Consortium Blockchains

Consortium blockchains sit between public and private, governed by a group of organizations rather than one entity or everyone.

Examples: Quorum, Hyperledger Besu, Energy Web Chain

Characteristics:

- Partially decentralized—multiple organizations share control

- More scalable than public blockchains

- Governance through consortium agreements

- Ideal for industry collaboration (banking, supply chain)

Immutability and Security: Why Blockchain Data Cannot Be Changed

The Concept of Immutability

Immutability means that once data is recorded on the blockchain, it cannot be altered or deleted. This isn’t enforced by rules or laws—it’s made practically impossible by mathematics and network design.

Why is blockchain immutable?

- Cryptographic linking: Each block references the previous block’s hash. Changing data changes the hash, breaking the chain.

- Distributed copies: Thousands of nodes store identical copies. An attacker would need to modify all of them simultaneously.

- Consensus rules: The network only accepts blocks following protocol rules. Invalid changes are rejected.

- Computational cost: In PoW, rewriting history requires re-doing all the computational work, faster than the entire network.

The 51% Attack

The main theoretical vulnerability is a 51% attack—if one entity controls more than half the network’s mining power (PoW) or staked tokens (PoS), they could potentially:

- Reverse recent transactions (double-spending)

- Prevent new transactions from confirming

- Exclude other miners from earning rewards

However, they CANNOT:

- Create new coins out of thin air

- Steal coins from addresses they don’t control

- Change consensus rules without network agreement

On major networks, 51% attacks are economically irrational—the cost would exceed any potential gain, and success would destroy confidence in the network, crashing the value of the attacker’s holdings.

Security Best Practices

While blockchain technology is secure, users must protect their own access:

- Secure your private keys: Never share them; use hardware wallets for significant holdings

- Verify addresses: Always double-check recipient addresses before sending

- Use reputable services: Interact only with audited smart contracts and established platforms

- Enable two-factor authentication: Add extra security layers to exchange accounts

Real-World Applications of Blockchain Technology

Cryptocurrency and Payments

The original blockchain application remains the most prominent. Cryptocurrencies enable:

- Borderless transactions without banks

- Near-instant international transfers

- Financial services for the unbanked

- Programmable money through smart contracts

Decentralized Finance (DeFi)

DeFi recreates traditional financial services—lending, borrowing, trading, insurance—on blockchain without intermediaries. The DeFi ecosystem includes:

- Decentralized exchanges (Uniswap, Curve)

- Lending protocols (Aave, Compound)

- Stablecoins (USDC, DAI)

- Yield farming and liquidity provision

Supply Chain Management

Major companies including Walmart, Maersk, and De Beers use blockchain to track products from origin to consumer. Benefits include:

- Instant traceability of product origins

- Reduced counterfeiting

- Faster recall response in food safety incidents

- Transparent sustainability verification

Healthcare

Blockchain applications in healthcare include:

- Medical records: Secure, patient-controlled health data

- Drug traceability: Tracking pharmaceuticals to prevent counterfeits

- Clinical trials: Immutable recording of research data

- Insurance claims: Automated processing via smart contracts

Digital Identity

Self-sovereign identity gives individuals control over their personal data. Instead of companies storing your information, you hold verifiable credentials and share only what’s needed. Use cases include:

- KYC/AML compliance without repeated identity verification

- Academic credential verification

- Government-issued digital IDs (Estonia’s e-Residency)

Voting and Governance

Blockchain-based voting could provide:

- Tamper-proof vote recording

- Instant, transparent result tabulation

- Remote voting with identity verification

- DAO governance for decentralized organizations

The Future of Blockchain Technology

Scalability Solutions

Current challenges around transaction speed and cost are being addressed through:

- Layer 2 solutions: Lightning Network (Bitcoin), Optimistic/ZK Rollups (Ethereum)

- Sharding: Dividing the network into parallel processing segments

- New consensus mechanisms: Innovations like Proof of History (Solana)

Interoperability

Projects like Polkadot, Cosmos, and cross-chain bridges are enabling different blockchains to communicate, moving toward a multi-chain future rather than winner-take-all.

Enterprise Adoption

Major corporations continue integrating blockchain for supply chain, payments, and data management. As the technology matures and regulatory frameworks develop, enterprise adoption is accelerating.

Central Bank Digital Currencies (CBDCs)

Over 130 countries are exploring or developing CBDCs—government-issued digital currencies often using blockchain or distributed ledger technology. China’s digital yuan is already in limited circulation.

Conclusion: The Building Blocks of a Decentralized Future

Blockchain technology represents a fundamental shift in how we record, transfer, and verify information. By combining cryptographic hashing, distributed networks, and consensus mechanisms, blockchain creates systems that are transparent, secure, and resistant to manipulation—all without requiring trust in any central authority.

Understanding how blockchain works—from transaction initiation through consensus and confirmation—reveals why this technology has captured the attention of developers, businesses, and governments worldwide. While challenges remain around scalability, regulation, and energy consumption, ongoing innovation continues to expand what’s possible.

Whether you’re interested in cryptocurrency investing, building decentralized applications, or simply understanding the technology shaping our digital future, the fundamentals covered in this guide provide the foundation for deeper exploration.

📚 Glossary

- Blockchain : A distributed digital ledger that records transactions across many computers in a way that makes the records difficult to alter retroactively. Data is stored in blocks that are cryptographically linked together.

- Block : A container of transaction data that includes a header (with metadata like the previous block’s hash) and a body (the actual transaction records). Blocks are added sequentially to form the blockchain.

- Cryptographic Hash : A mathematical function that converts input of any size into a fixed-length string of characters. It’s one-way (cannot be reversed) and collision-resistant (virtually impossible to find two inputs producing the same output).

- Node : A computer that participates in the blockchain network by storing a copy of the ledger and validating transactions. Full nodes store the complete blockchain history.

- Consensus Mechanism : The protocol by which a distributed network agrees on the current state of the blockchain. Common mechanisms include Proof of Work and Proof of Stake.

- Proof of Work (PoW) : A consensus mechanism where miners compete to solve computational puzzles to validate transactions and create new blocks. Used by Bitcoin.

- Proof of Stake (PoS) : A consensus mechanism where validators are selected based on the amount of cryptocurrency they stake as collateral. More energy-efficient than PoW. Used by Ethereum.

- Decentralization : The distribution of control and data across many participants rather than a single central authority. A key property that makes blockchain censorship-resistant.

- Immutability : The property that makes blockchain data permanent and unalterable once recorded. Achieved through cryptographic linking and distributed consensus.

- Smart Contract : Self-executing code stored on a blockchain that automatically enforces the terms of an agreement when predetermined conditions are met.

- Private Key : A secret cryptographic code that proves ownership of blockchain assets and enables transaction signing. Must be kept secure and never shared.

- Distributed Ledger : A database shared and synchronized across multiple locations, institutions, or geographies, accessible by multiple people. Blockchain is a type of distributed ledger.

- Mempool : The waiting area where unconfirmed transactions queue before being included in a block. Miners/validators select transactions from the mempool.

- Nonce : “Number used once” – a value miners adjust when attempting to find a valid block hash in Proof of Work mining.

- DeFi (Decentralized Finance) : Financial services built on blockchain technology that operate without traditional intermediaries like banks, using smart contracts instead.

- Wallet : Software or hardware that stores private keys and enables users to send and receive cryptocurrency. Wallets don’t actually “store” crypto—they store the keys that prove ownership.

Frequently Asked Questions

What is the difference between blockchain and cryptocurrency?

Blockchain is the underlying technology—a distributed ledger that records data in linked blocks. Cryptocurrency (like Bitcoin or Ethereum) is one application of blockchain technology, specifically used for digital money transfers. Think of blockchain as the foundation and cryptocurrency as one building constructed on that foundation. Blockchain can be used for many purposes beyond cryptocurrency, including supply chain tracking, voting systems, and digital identity management.

Can blockchain be hacked or tampered with?

While no system is 100% hack-proof, blockchain is extremely secure by design. Altering data on a major blockchain would require controlling more than 50% of the network’s computing power (for PoW) or staked tokens (for PoS), recalculating all subsequent blocks, and doing this faster than the rest of the network adds new blocks. On networks like Bitcoin with thousands of nodes and enormous hash power, this is practically impossible and economically irrational—the attack cost would exceed any potential gain.

How long does a blockchain transaction take?

Transaction times vary by blockchain. Bitcoin averages one block every 10 minutes, with 6 confirmations (approximately 1 hour) considered secure for large transfers. Ethereum produces blocks every 12 seconds with faster finality. Newer blockchains like Solana can process thousands of transactions per second with near-instant confirmation. Transaction fees and network congestion also affect processing times.

What is the environmental impact of blockchain?

Environmental impact varies dramatically by consensus mechanism. Proof of Work blockchains like Bitcoin consume significant electricity (comparable to some small countries) because miners run energy-intensive hardware. Proof of Stake blockchains use 99%+ less energy—Ethereum’s transition to PoS reduced its energy consumption by approximately 99.95%. Many newer blockchains are designed with sustainability in mind, and Bitcoin mining increasingly uses renewable energy sources.

Do I need to understand blockchain to use cryptocurrency?

Not necessarily. Just as you don’t need to understand TCP/IP to browse the internet, you can use cryptocurrency without deep technical knowledge. User-friendly wallets and exchanges handle the complexity. However, understanding blockchain basics helps you make informed decisions, recognize scams, and appreciate why cryptocurrency has value. The more you understand, the safer and more effective your participation will be.

What happens if I lose my private key?

Losing your private key means permanently losing access to your cryptocurrency—there’s no “forgot password” option or customer support to recover it. This is why secure backup is crucial: write down your recovery phrase (seed phrase), store it in multiple secure physical locations, and consider using a hardware wallet for significant holdings. The immutability that makes blockchain secure also means no one can reverse a lost key situation.

Is blockchain technology legal?

Blockchain technology itself is legal virtually everywhere. However, regulations around cryptocurrency usage, trading, and taxation vary significantly by country. Some nations embrace crypto (El Salvador made Bitcoin legal tender), while others restrict or ban certain activities. Always research your local laws regarding cryptocurrency taxation, trading, and reporting requirements. The technology continues to gain regulatory acceptance as frameworks mature.

Can blockchain work without cryptocurrency?

Yes, absolutely. While cryptocurrency was blockchain’s first application, the technology works independently. Private and consortium blockchains used by enterprises often don’t have associated cryptocurrencies. Applications include: supply chain tracking at Walmart, cross-border payments at major banks, medical records management, and land registry systems in multiple countries. Cryptocurrency is just one use case among many.

📰 Sources

This article is based on the following sources:

- Bitcoin Whitepaper by Satoshi Nakamoto

- Ethereum Documentation

- IBM Blockchain Explained

- Cambridge Bitcoin Electricity Consumption Index

- Investopedia Blockchain Guide

- Ethereum Energy Consumption Report

- World Economic Forum Blockchain Report

Comment citer cet article : Fibo Crypto. (2026). How Does Blockchain Work? Complete Guide to Blockchain Technology [2026]. Consulté le 4 March 2026 sur https://fibo-crypto.fr/en/blog/how-blockchain-works