What Is Aave? Complete Guide to the Leading DeFi Protocol

📋 En bref (TL;DR)

- Definition: Aave is the largest decentralized lending and borrowing protocol (DeFi), allowing users to deposit crypto to earn interest or borrow by depositing collateral

- How it works: Users deposit into liquidity pools and receive aTokens generating interest; borrowers deposit collateral exceeding the borrowed amount (overcollateralization)

- Innovations: Flash loans (instant loans without collateral), GHO (native stablecoin), Efficiency mode for correlated assets, multi-chain support

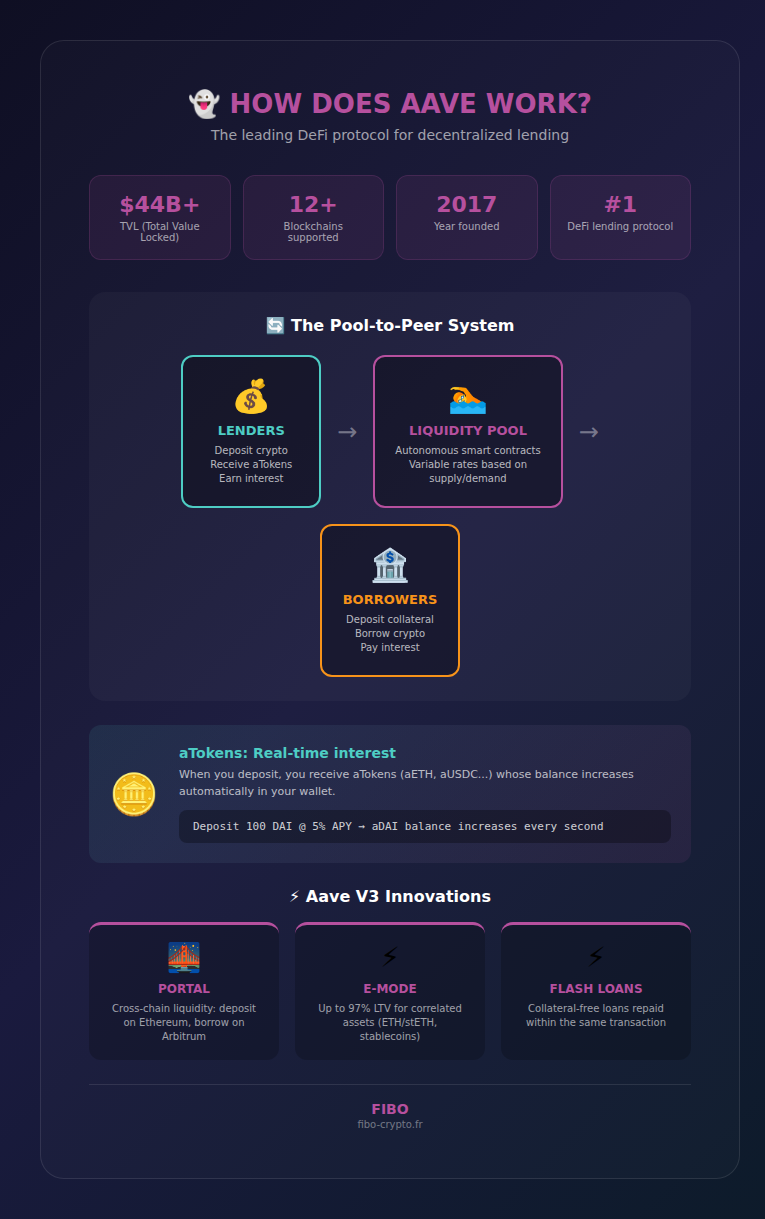

- Key figures: Over $44 billion in TVL, available on 12+ blockchains, undisputed leader in DeFi lending

- AAVE token: Protocol governance, staking in the Safety Module, discounts on GHO borrowing

- Key takeaway: Aave makes traditional banking services accessible without intermediaries, with complete transparency and control over your assets

In the world of decentralized finance (DeFi), Aave has established itself as the go-to protocol for cryptocurrency lending and borrowing. With over $44 billion deposited and a presence on more than 12 blockchains, Aave is transforming how users access financial services — without banks, without paperwork, and while maintaining complete control over their assets.

What Is Aave?

Aave is a decentralized finance protocol that allows anyone to lend or borrow cryptocurrencies without going through a bank or intermediary. The name “Aave” means “ghost” in Finnish, a nod to the transparent and immaterial nature of the protocol.

2x cheaper fees. Up to 6% yield. No seed phrase. Fibo, the wallet you've been waiting for.

Get early access →Unlike traditional banks where a central institution manages your money, Aave operates through smart contracts — autonomous computer programs that automatically execute lending and borrowing operations. Everything is transparent, verifiable on the blockchain, and accessible 24/7.

Founded in 2017 under the name ETHLend by Stani Kulechov, a Finnish law student, the project raised $16.2 million during its ICO. In 2018, ETHLend became Aave and adopted the liquidity pool model that made it successful.

How Does Aave Work?

Aave works through liquidity pools: lenders deposit their crypto into these shared pools, and borrowers can draw from them by depositing collateral. It’s a “pool-to-peer” system rather than “peer-to-peer” — you’re not lending directly to a person, but to a pool accessible to everyone.

For Lenders (Suppliers)

When you deposit cryptocurrencies on Aave:

- You receive aTokens in exchange (for example, aETH for deposited ETH)

- These aTokens continuously generate interest automatically

- The interest rate varies based on supply and demand for the asset

- You can withdraw your funds at any time (if liquidity is available)

aTokens are fascinating: their balance increases directly in your wallet over time. If you deposit 100 DAI and the rate is 5% annually, you’ll see your aDAI balance gradually increase.

For Borrowers

To borrow on Aave, you must:

- Deposit collateral: crypto worth more than what you want to borrow

- Respect the LTV ratio (Loan-to-Value): typically 75-80% maximum

- Monitor your “health factor”: if your collateral loses too much value, it can be liquidated

Why borrow rather than sell? Imagine you have ETH and believe its price will rise, but you need liquidity. By borrowing stablecoins against your ETH, you maintain your exposure to potential upside while obtaining funds.

Overcollateralization: Why Deposit More Than You Borrow?

Overcollateralization is Aave’s fundamental security mechanism: you must deposit collateral exceeding your loan value (typically 125-200%) to protect the protocol against defaults.

If your collateral price drops too much relative to your loan, Aave triggers a liquidation: part of your collateral is automatically sold to repay the loan and protect lenders.

Each asset has a different liquidation threshold. For example, ETH might have a threshold of 82.5%, meaning if your loan/collateral ratio exceeds 82.5%, you risk liquidation.

Aave V3: Major Innovations

Launched in March 2022, Aave V3 represents a major evolution of the protocol with three revolutionary features:

Portal: Borderless Liquidity

Portal allows moving liquidity between different blockchains seamlessly. You can deposit on Ethereum and borrow on Polygon or Arbitrum, without having to manually transfer your assets.

Efficiency Mode (E-Mode)

E-Mode allows borrowing more when your collateral and loan are correlated assets. For example, if you deposit stETH to borrow ETH, you can reach an LTV ratio up to 97% instead of the usual 80%.

It’s ideal for:

- Stablecoin pairs (USDC/DAI/USDT)

- ETH derivatives (ETH/stETH/wstETH)

- Sophisticated trading strategies

Isolation Mode

When Aave lists a potentially riskier new asset, it can be placed in “isolation mode.” This limits which assets you can borrow with that collateral and caps the total borrowable amount.

Flash Loans: Borrowing Without Collateral

Flash loans are Aave’s most audacious innovation: instant loans without any collateral, provided repayment occurs within the same blockchain transaction. Aave was the first protocol to offer this feature in 2020.

How is this possible? In a blockchain, a transaction is either entirely executed or entirely reverted. A flash loan exploits this property:

- You borrow millions of dollars in crypto

- You perform your operations (arbitrage, refinancing, etc.)

- You repay the loan + fees (0.09%)

- If repayment fails, the entire transaction is reverted

GHO: Aave’s Decentralized Stablecoin

GHO is Aave’s native stablecoin, launched in 2023. Unlike regular loans where interest goes to lenders, 100% of interest paid on GHO goes directly to the Aave DAO treasury.

To get GHO, you deposit collateral on Aave and “mint” (create) GHO. The process is similar to DAI:

- Overcollateralization required

- Interest rate set by governance

- Price pegged to $1 (no oracle dependency for price)

A key advantage: staked AAVE holders (stkAAVE) benefit from a reduced rate when borrowing GHO.

The AAVE Token: Governance and Utility

AAVE is the protocol’s governance token. Each token represents a vote to decide Aave’s future: new assets, risk parameters, treasury usage, etc.

1. Governance

AAVE holders can vote on Aave Improvement Proposals (AIPs). The Aave DAO is one of the most active in the DeFi ecosystem.

2. Staking in the Safety Module

You can stake your AAVE in the Safety Module, a security mechanism that protects the protocol. In return, you receive AAVE rewards. Warning: in case of a major issue, up to 30% of staked AAVE can be liquidated to cover losses.

3. Benefits for Borrowers

Using AAVE as collateral provides discounts on borrowing fees. stkAAVE stakers also benefit from preferential rates on GHO.

On Which Blockchains Is Aave Available?

Aave is deployed on more than 12 blockchains, making it one of the most accessible DeFi protocols:

- Ethereum (mainnet)

- Polygon

- Arbitrum

- Optimism

- Avalanche

- Base

- BNB Chain

- Fantom

- Metis

- Gnosis

- Scroll

- zkSync

This multi-chain presence allows users to choose the network based on transaction fees and available liquidity.

Risks to Know

Like any DeFi protocol, Aave carries risks:

- Liquidation risk: If your collateral loses value, you can be liquidated

- Smart contract risk: Potential bugs in the code (though Aave is extensively audited)

- Oracle risk: Dependency on external price feeds (Chainlink)

- No government insurance: Unlike bank deposits

📚 Glossary

- DeFi protocol : Decentralized application offering financial services (lending, exchanging, etc.) without intermediaries, via smart contracts on blockchain.

- Smart contract : Autonomous computer program deployed on a blockchain, automatically executing actions according to predefined conditions.

- Liquidity pool : Reserve of cryptocurrencies deposited by users, enabling exchanges or loans on a DeFi protocol.

- aToken : Token representing a deposit on Aave. Its balance automatically increases over time according to generated interest.

- LTV (Loan-to-Value) : Ratio between borrowed amount and deposited collateral value. A 75% LTV means you can borrow up to 75% of your collateral’s value.

- Overcollateralization : Requirement to deposit collateral exceeding the borrowed value to guarantee repayment and protect lenders.

- Flash loan : Instant loan without collateral, provided it’s repaid within the same blockchain transaction. Used for arbitrage and refinancing.

- GHO : Aave’s native decentralized stablecoin, created by depositing collateral. Interest goes to the DAO treasury.

- AAVE (token) : Aave protocol’s governance token, allowing voting on proposals and staking in the Safety Module.

- Safety Module : Aave protection mechanism where holders stake their AAVE to secure the protocol in exchange for rewards.

- TVL (Total Value Locked) : Total value of assets deposited in a DeFi protocol. Indicator of protocol size and trust.

- Health Factor : Health indicator of a borrowing position on Aave. Below 1, the position risks liquidation.

Frequently Asked Questions

Is Aave safe?

Aave is one of the most audited and battle-tested DeFi protocols, with over $44 billion in TVL. It has survived several market crashes without major incidents. However, like any DeFi protocol, it carries risks (smart contracts, liquidations). Only invest what you can afford to lose.

How do I earn interest on Aave?

Simply deposit your cryptocurrencies on Aave (via app.aave.com). You’ll receive aTokens whose balance automatically increases according to the variable interest rate. Rates depend on supply and demand for each asset — stablecoins typically offer 2-8% APY.

What's the difference between Aave and Compound?

Aave and Compound are both lending protocols, but Aave offers more features: flash loans, E-Mode, multi-chain support, and the GHO stablecoin. Aave also has higher TVL and a greater variety of supported assets.

Can I get liquidated on Aave?

Yes, if your collateral value drops and your health factor falls below 1, part of your collateral will be sold to repay your debt. To avoid this, monitor your health factor and maintain a safety margin (ideally > 1.5).

What is a flash loan and what is it used for?

A flash loan is an instant loan without collateral, repaid within the same blockchain transaction. It’s used by traders for arbitrage (profiting from price differences between platforms), position refinancing, or liquidations. This requires advanced technical skills.

📰 Sources

This article is based on the following sources:

Comment citer cet article : Fibo Crypto. (2026). What Is Aave? Complete Guide to the Leading DeFi Protocol. Consulté le 24 March 2026 sur https://fibo-crypto.fr/en/blog/what-is-aave-complete-guide/

The simplest way to buy, swap and manage your crypto

Join the first users and get priority access. No seed phrase, fees 3.5x lower, built-in DeFi yield.

Get early access →